CNA Explains: Why are Singapore Savings Bonds in hot demand and should you invest in them?

Rising yields from the Singapore Savings Bonds have been attracting more investors in recent months. Is it too late for you to jump in? CNA asks the experts.

Singapore dollar notes. (File photo: AFP/Roslan Rahman)

SINGAPORE: Amid the search for returns and safety in a volatile market, one investment product has been gaining attention of late – the Singapore Savings Bonds.

The August tranche received applications worth S$2.4 billion, the highest since the savings bond was launched in 2015 and up from S$1.3 billion in the previous tranche.

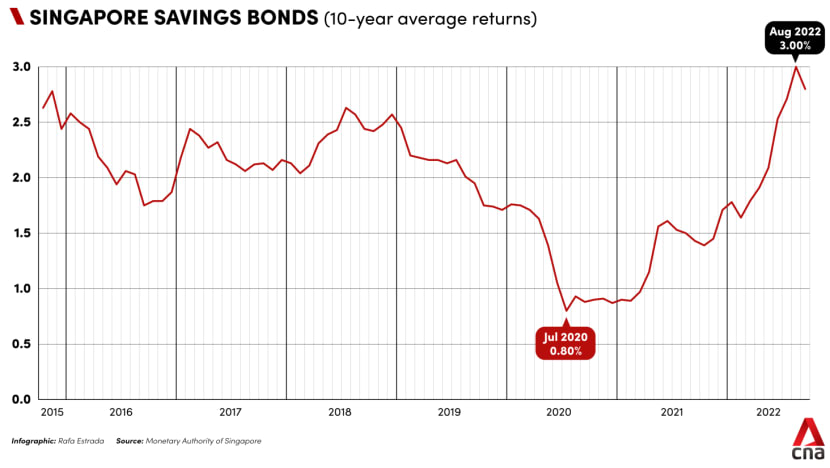

The rush into the bonds comes as its 10-year average return has been on the rise – hitting a record high of 3 per cent in the August issue.

Applications for the September tranche are under way until Aug 26. Offering a 10-year average return average of 2.8 per cent, it is expected to receive a healthy amount of demand.

Here’s what you need to know about the Singapore Savings Bonds:

A QUICK INTRODUCTION

First launched in 2015, the Singapore Savings Bonds are a type of Singapore Government Securities (SGS), meaning they are issued and guaranteed by the Singapore Government.

New tranches are released at the start of each month, with fixed interest rates that step up for each year they are held and locked in for 10 years.

Investment amounts start from S$500 and can be made via cash or Supplementary Retirement Scheme funds. A S$2 transaction fee applies for each application.

After the saving bond is issued, interest will be paid out every six months.

Unlike regular SGS bonds, the Singapore Savings Bonds are not tradable on the open market.

WHY ARE RETURNS GOING UP?

The interest rates of each Singapore Savings Bond issuance are based on the average SGS yields in the month before applications open.

These yields have been on an uptrend like all other major economies’ bond yields, as global central banks raise interest rates and mull other ways of normalising monetary policy to combat surging inflation, said MoneyOwl’s chief executive and chief investment officer Chuin Ting Weber.

The US Federal Reserve, for one, has delivered four rate hikes this year.

Against that backdrop, the 10-year average return for the Singapore Savings Bonds issued this year has risen from 1.78 per cent in January to a record 3 per cent in August.

While the average rate dipped slightly to 2.8 per cent for the September issue, it remains the second highest so far in 2022. The latest tranche also offers an interest rate of 2.63 per cent for the first year, markedly above the first-year rates of past tranches.

Where the interest rates for future Singapore Savings Bonds are headed will depend on the trajectory of inflation and central bank actions, said Mrs Weber.

“If policy tightening can bring down inflation rapidly, possibly together with the easing of other supply chain factors, rates may stop increasing. In fact, if recession sets in because of the tightening and inflation peaks, policymakers may cut rates in the future to support the economy,” she explained.

Mr Victor Wong, director of wealth management at Financial Alliance, suggested looking at the US 10-year bond yield for some guidance. The yield on the benchmark 10-year bond has been falling since the US central bank’s latest 75-basis-point rate hike.

“Singapore’s 10-year bond interest rate generally follows the direction of the US 10-year bond,” he said. “Hence, I would not be surprised if the upcoming issues offer lower average 10-year interest rates.

“But the first-year yield could be higher or remain the same since Singapore’s short-term rates also usually follow the direction of US short-term rates, which have risen.”

THE PROS AND CONS

Given that investors can put in as little as S$500, the Singapore Savings Bonds are an accessible option for most people, financial experts told CNA.

It is “almost” risk-free as it is fully backed by the Singapore Government, according to Providend’s client adviser Bryan Chan. And because the Singapore Savings Bonds are not traded, capital put in is not affected by interest rate fluctuations, meaning that investors will always get back their principal.

Most importantly, investors are free to withdraw or redeem the savings bond at any time even though the product is issued with a 10-year maturity term. There are no penalties involved and accrued interest will not be forfeited, unlike other fixed income products such as fixed deposits, experts said.

To be sure, the Singapore Savings Bonds are not without drawbacks.

One is that withdrawals are not immediate and can take up to 30 days, Mr Chan said.

The non-refundable administrative fee of S$2 for applications and redemptions before the 10-year maturity may also eat into the returns of those investing very small amounts, noted Mrs Weber.

“And if you try to ‘churn’ the Singapore Savings Bonds – redeeming lower interest ones to apply for new issues – you will incur these fees,” she added.

Lastly, given the strong demand of late, investors are unlikely to get the full amount they applied for even if they remain well within the individual limit of S$200,000 held across different tranches.

The quantity ceiling – applied when applications exceed the issuance size – for the August issue was S$9,000, versus the S$18,000 limit in the previous month.

“So even if you have money, you may not be able to invest in a meaningful way,” Mr Wong said.

.jpg?itok=RNQV2h7x)

HOW TO INVEST

So how should one go about approaching the Singapore Savings Bonds?

Mr Chan said bonds and lower-risk investment products largely act as “stabilisers” in an investment portfolio. While different instruments offer varying degrees of safety and returns, they typically help to moderate overall risks by providing stable returns for a portion of the portfolio.

Hence, the Singapore Savings Bonds can be a place to park funds that must be kept safe in the short term given but do not need to be used that urgently given the wait time of at least 30 days, he added.

As for how much to invest, experts said that depends on factors such as one’s risk appetite and overall portfolio size.

For those with a large investment portfolio and are looking for lower-risk alternatives, “going as far as the limit of S$200,000 is not unreasonable, especially if that represents a relatively small part of the portfolio”, said Mr Chan.

“If they require a higher return, have a long-time horizon and are willing to take on more risk, then they may want to prioritise allocating their investment funds to other things such as equities,” he added.

Age could also be a consideration when it comes to deciding on asset allocations, although Mrs Weber stressed that the ability to take risks is “not age per se” but one’s time horizon.

“The longer the period of time you have between now to when you need the money, the larger the proportion of equities you can have in your portfolio because you have the ability to stay through short-term downturns without having to liquidate it,” she explained.

“If you are looking to use a bucket of funds in the next one to five years – and this can be income for living expenses for retirees or saving for a property for young persons – you do not want to take big risks with this sum of money.

“The Singapore Savings Bonds can be suitable for you, alongside other low-risk instruments like fixed deposits, short duration, high-quality bond funds or annuities.”

One might also wonder if a lump-sum or “laddering” approach would work better for the Singapore Savings Bonds.

Again, experts said there is no one-size-fits-all strategy given the smaller allotments in recent issues due to strong demand. Also, as interest rates trend higher, other more attractive options might emerge.

For example, banks in Singapore have been raising their rates for fixed deposits, while some robo-advisers like StashAway are also starting to increase interest rates for their cash-management accounts.

Mr Wong said: “My view is that we could be near the peak of the current interest rate cycle, provided inflation does not stay elevated for a prolonged period. Hence, lump sum investments could be preferred to lock in the current yield.

“But again, your investments could be hampered by reduced allocation … so you may have to subscribe to many subsequent issues if you want to employ a meaningful amount in the Singapore Savings Bonds.”

But ultimately, with returns from lower-risk options unlikely to keep pace with inflation, investors may need to take some risk in their portfolios such as by having a comfortable mix of equities and bonds, Mrs Weber said.

“Staying invested in a suitable portfolio is the best way to reach your goals in your time frame. You need to ride out the volatility to capture the recovery and reap the long-term returns.”