Healthcare costs are rising in Singapore. Is there really nothing we can do about it?

Healthcare spending is growing, along with government subsidies — owing to an ageing population, medical advances and increased operational costs. Here are some steps being taken to help people cope, and how the public can play a part.

Manpower accounts for about 60 per cent of healthcare costs in hospitals — and a staff shortage is pushing up wages.

This audio is generated by an AI tool.

In partnership with the Ministry of Health

SINGAPORE: Before the pandemic, Hariati Abdul Muhin liked her shopping — retail therapy, she calls it — and her Malaysian holidays.

While the border closures put a halt to her short trips, another development emerged that made shopping difficult too: knee trouble. “When I walked … it’d cause a lot of pain,” recalled the 51-year-old. “It felt like the bones were brushing against (each other).”

A polyclinic doctor gave her a referral to an orthopaedic specialist at the National University Hospital (NUH). A scan showed that the cartilage in her knees was thinning.

Discovering that knee replacement surgery was an option at age 48 came as “quite a surprise” — but she was not alone in that.

Nowadays, “a small but significant proportion of patients” in their late 40s or their 50s have “serious knee pain”, said NUH senior consultant Chua Wei Liang, who heads the hospital’s division of adult reconstruction and joint replacement surgery.

Indeed, knee replacement is “one of the more common surgeries” in Singapore. Across NUH and Alexandra Hospital (AH), for example, there are more than 1,000 cases a year, he cited.

Awareness of the treatment options is one factor behind this. Technological advances are another. “The (implant) materials have improved,” said Chua. Durability and success rates have improved with better instrumentation.

“With better painkillers, better pain management methods, … instead of having to suffer in hospital for over a week, (in) two or three days’ time (patients) will say to you, ‘Doc, I’m okay, I can manage at home.’”

In Hariati’s case, she stayed in hospital for one night, in Class C, when she had her first knee replacement. Her hospitalisation bill was mostly covered by subsidies and MediShield Life, and her out-of-pocket expenses were below S$1,000.

While it was something she could afford, the common procedure has got more expensive with all the medical advances.

Ten to 15 years ago, knee implants cost between S$3,000 and S$3,500, said Chua, who treated Hariati. Today, the cost is about S$4,500 to S$5,000.

Rising healthcare costs have come sharply into focus in recent times, with Health Minister Ong Ye Kung describing the issue as a pressing one during his ministry’s budget debate earlier this year.

The rising costs are having an impact not only on major health episodes such as critical illnesses, but also on high-volume surgeries like knee replacements.

And advances in medical technology are not the only reasons costs have increased. Operational costs are a contributing factor, along with overly generous private insurance coverage.

So what is being done to manage some of these costs or to help Singaporeans cope — and what can individuals do on their part?

WATCH: Why are healthcare costs rising in Singapore — is there really nothing we can do about it? (12:55)

PRESSURE POINTS FOR HOSPITALS

The largest portion of Singapore’s healthcare costs, at 60 per cent, is the cost of manpower.

And a shortage of manpower is pushing up wages, said Wong Soo Min, the group chief financial officer of the National University Health System, which manages NUH, AH, Ng Teng Fong General Hospital and National University Polyclinics, among other healthcare institutions.

Drugs, consumables and information technology-related costs account for the remaining 40 per cent of healthcare costs. “With inflation as well as higher logistics and supply chain costs, we do see higher drug costs,” she added.

While these higher operating expenses are putting pressure on hospitals, healthcare administrators are looking at ways to proactively manage costs.

One of the things they are doing is “switching from branded to generic drugs, with the same efficacy”, said Wong.

She cited two examples — cholesterol and hypertension drugs — where the switch has led to cost savings of about 20 per cent. “And this gets translated into the price that the patient pays,” she added.

Technology offers another set of solutions when it comes to manpower efficiency. For example, AH is piloting smart wards with digital wearables for patients and beds equipped with contactless sensors to monitor the patients.

If their vital signs are not normal, this will activate an alarm signal, and the nurses can check on the patient, said Wong. In a traditional ward, one nurse typically handles five beds. But in this smart ward, a nurse can manage six, boosting efficiency by 20 per cent.

Some factors in healthcare costs, however, are beyond the hospitals’ control. The ageing population is one: Today, one in five Singaporeans are aged 65 and over. By 2030, nearly one in four will be a senior.

“As the population collectively ages, we then have many more individuals who have chronic disease,” said Jeremy Lim, an associate professor at the National University of Singapore’s Saw Swee Hock School of Public Health.

“This then imposes a very heavy burden on the healthcare system.”

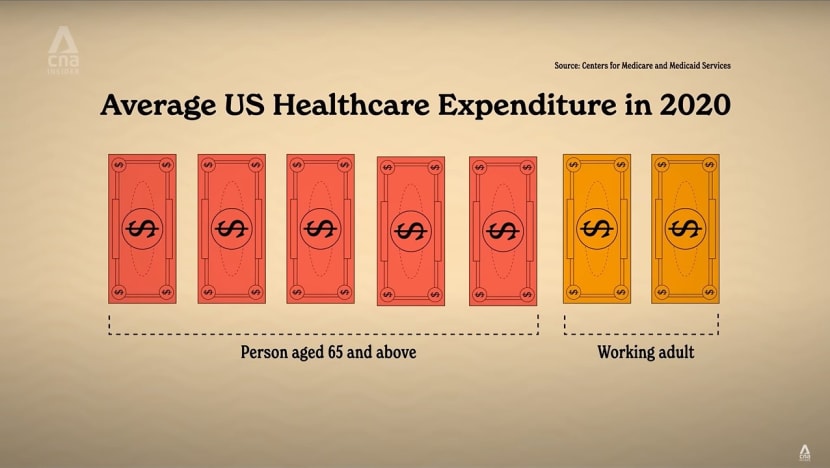

According to data in the United States, healthcare spending per person for those aged 65 and over is 2.5 times the spending per working-age person. In South Korea, the healthcare spending on seniors is four times higher per person than on those below age 65.

SINGAPORE’S HEALTHCARE “BUCKETS”

In Singapore, the healthcare bill is paid using a combination of methods. One is through subsidies funded by government revenue such as taxes.

The second is through MediShield Life, the national health insurance scheme funded by the premiums that all residents pay. The third is through MediSave, the national medical savings scheme.

The government accounts for more than half of all spending, while more than a fifth comes from patients’ out-of-pocket payments.

“When we have many more mechanisms or buckets to pay for healthcare, the system then becomes more resilient,” said Lim. “Think of it as an aeroplane with four engines rather than two.

If one is down, then the others could step up.”

On the other hand, if healthcare is “free” at the point of delivery, “there’ll be overconsumption”, he said. “Doctors and their patients (will) choose the most expensive interventions when a less expensive one would do just as well.

“We’ll spend more on medicines than we’d actually need to. … We’ll get more unsustainable even more quickly.”

If healthcare financing were entirely dependent on residents buying private insurance, like in the US, then society risks being split into the haves and the have-nots, he said.

“(The haves) will have much greater access to … drugs or therapies that may not be available to those who don’t have insurance, because these are priced at such a level that, realistically, paying … out of pocket is just not possible.”

Singapore’s MediShield Life covers all residents, protecting against large medical bills for life regardless of pre-existing conditions.

As a basic health insurance plan, however, it excludes lower-cost treatment and services, such as consultations with a general practitioner, among other exemptions.

The key thing to look at when it comes to the MediShield Life Fund, said Lim, is whether it is “collecting the right amount of premiums relative to the claims”.

“In terms of the efficiency, none of us want to pay more premiums than we have to,” he noted.

According to Ministry of Health (MOH) data, the fund’s average operating loss ratio between 2020 and last year was 100 per cent.

This means that on average, the total premiums collected matched the total monies required to meet liabilities, including claims expected to be paid in future.

GOVERNMENT MEASURES TO DEAL WITH COSTS

The rising healthcare costs, however, have eroded the coverage provided by MediShield Life’s existing claim limits — which together with MediSave, fully cover just under eight in 10 subsidised bills today.

This is lower than the nine in 10 subsidised bills MediSave and MediShield Life were designed to cover. So, from next April, premiums will increase by up to 35 per cent (on average, 22 per cent per policyholder) over a three-year period to allow for higher claim limits.

Beyond that, coverage will also be expanded to include more treatments. “We’re seeing a wave of new therapies being developed. They’re called cell, tissue and gene therapies (CTGTPs),” cited MOH deputy secretary (policy) Jasmin Lau.

“These developments do give hope to people with rare conditions. I think it’s only right for a national insurance scheme to provide some support.”

LISTEN: A breakdown of the MediShield Life changes — How to save on medical costs

New outpatient treatments and home-based medical care will also be covered going forward. “Some patients … need a respiratory support system. And these ventilation systems can be provided in a hospital, or they can be used at home,” she said.

“It helps to manage healthcare costs because the cost of an inpatient stay is a lot more than if they were to stay at home.”

In recent years, the government has also been providing more subsidies for medical care. In 2016, MOH’s healthcare spending was about S$10 billion. Last year, it was about S$18 billion.

To help deal with the rising costs, the Agency for Care Effectiveness conducts technical evaluations that inform the government’s funding decisions and coverage for clinically and cost-effective health technologies, such as drugs, vaccines, CTGTPs and medical devices.

“About 40 or 50 new drugs will enter the Singapore market each year. And we do an evaluation of the drugs we should subsidise … based on the data that’s been published so far,” said the agency’s executive director, Daphne Khoo.

“If I were to spend S$1 million on this drug, how many more healthy life years would I buy for the population?”

In addition, her team negotiates with pharmaceutical and medical technology companies to get the best prices for drugs and medical technologies.

“In the past, the company came to you and said … ‘We’re going to charge S$1,000 for this drug.’ And we either said yes or no,” she recounted.

Now we say that based on our analyses, ‘it’s not very cost effective, so … can you come back with a better price?’”

The agency’s work helps healthcare practitioners such as Jen Wei Ying, a consultant at the National University Cancer Institute, Singapore, to formulate cost-effective treatment plans that work well for patients.

“We can usually reassure patients that there’ll be subsidies for the initial treatment of most cancers, which minimises the out-of-pocket costs for the majority of patients,” said the doctor.

“LAST PIECE OF THE PUZZLE”

Managing the cost of drugs and medical technologies is not the only way to contain healthcare costs. Where patients go to receive treatment — for example, for high blood pressure, or hypertension — makes a difference too.

“Many family physicians are well trained to manage (cases) within the community and within the clinics, in a primary care setting,” said S Suraj Kumar, a senior family physician from Drs Bain and Partners. “And it reduces costs.”

General practitioners can also continue the care of patients who have been hospitalised and are stable enough to leave, such that “there’s no break in the journey or the medical treatment”, he added.

“The shorter the amount of time they spend in hospitals, the better in terms of cost.”

Singaporeans can start seeing a family doctor through Healthier SG, a national programme that adjunct senior research fellow Phua Kai Hong at the Institute of Policy Studies sees as the “last piece of the puzzle of healthcare financing”.

Through this initiative, doctors are reimbursed based on the number of enrolled patients in their care.

The aim is preventive care. “We look after (patients’) health needs to make sure they lead a healthy life. We detect problems early, and we can manage them,” said Kumar. Based on a patient’s medical history, the doctor may recommend certain health screenings.

For those who are enrolled in Healthier SG, there are free screenings at their participating clinic for some chronic conditions and cancers: type 2 diabetes; hypertension; hyperlipidaemia, or high cholesterol; breast cancer; cervical cancer; and colorectal cancer.

Cervical cancer screening, for example, is recommended for females aged 25 and over, while screening for chronic illnesses is advised for males and females aged 40 and over.

For her part, Hariati has learned from her knee replacement surgeries that it is never too early to make lifestyle changes, like losing 19kg in weight.

“If I want to travel, I need good legs. Of course I need good knees,” she said. These days she is “definitely happy” and can “look forward to going anywhere”.

“My husband always makes a point of, on weekends, going out with my children,” she shared. “I want to join (in) the fun. … For me, nothing (else) matters. It’s family.”

.jpg?itok=IduGQxVf)