commentary Commentary

Commentary: Hawkers want to embrace cashless payments but say they need help tackling barriers

Hawkers face four kinds of barrier to adopting cashless payments; government initiatives should focus on targeting a few, say two SUSS observers.

Diners at the hawker centre at Our Tampines Hub. (File photo: Fann Sim)

SINGAPORE: Cash may be king in the past but if Singapore aims to be a leading digital economy, there is no running away from going cashless, whether we like it or not.

A digital economy — a key element in Singapore’s metamorphosis into a Smart Nation — is impossible without the development of a first-class payment ecosystem that is efficient, secure and allows people to make seamless mobile transactions.

The Singapore Government has been encouraging the adoption of cashless modes of payment across various domains and industries, including the food and beverage (F&B) sector.

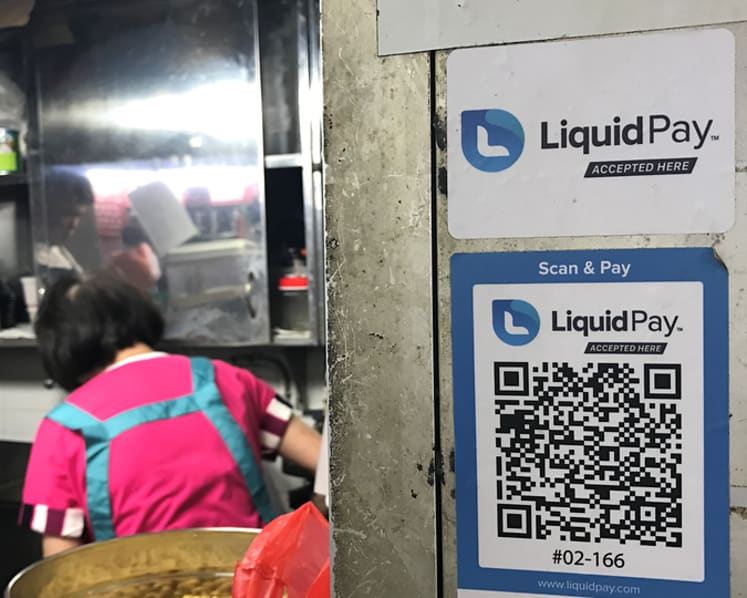

Many mobile payment platforms have also been introduced by different providers, such as NETsPay, GrabPay, LiquidPay, DBS PayLah!, PayNow, Google Pay, Apple Pay and Samsung Pay.

PERSISTENTLY LOW ADOPTION OF CASHLESS PAYMENTS

However, despite the introduction of many initiatives to push the economy towards cashless transactions, usage rates remain persistently low compared to cash payments, especially in small business establishments, small F&B outlets and hawker centres.

READ: Beneath the digital friendly facade, Singaporeans still reluctant to accept cashless payment, a commentary

A 2016 KPMG study found that nine out of 10 consumers still prefer to pay in cash in wet markets and hawker centres in Singapore. About 90 per cent of transactions were transacted in cash in wet market and hawker centres.

In other F&B businesses, cash transactions were fewer, with fast-food outlets at about 55 per cent, and dine-in restaurants at less than 20 per cent.

These findings suggest that small business establishments and hawkers view mobile payments as a complementary payment method and not a substitute.

A survey conducted for a Singapore University of Social Sciences’ student project in September this year suggested that this preference for cash has remained unchanged, and more needs to be done to break down hurdles hawkers face.

Out of 236 hawkers polled across hawker centres in Singapore, only 39.8 per cent said they accepted mobile payments, while the remaining 142 had yet to accept mobile payments.

Among those who accepted mobile payments, only 19.6 per cent of them had been using mobile payment for more than one year; while 48.9 per cent had been using mobile payments between six months and one year. The rest said they had used it for less than six months.

FOUR BARRIERS FOR HAWKERS

Though the push towards cashless has been accelerated in recent months, including the appointment of NETS to unify the fragmented payments landscape and bring cashless to hawker centres, canteens and coffee shops, the SUSS student survey suggests that the state of mobile payments among hawkers is still in its infant stages.

This is not surprising since hawkers, in general, are senior citizens, relatively less educated and less technology savvy. And press reports have also noted that hawkers prefer to have cash in hand because most of their suppliers also demand cash.

These factors aside, hawkers’ lack of enthusiasm in adopting mobile payment can also be attributed to four barriers: Cost barriers, tradition barriers, usage barriers and value barriers.

Cost barriers refer to additional costs incurred in adopting mobile payment services, including the cost of getting a smartphone and the incurrence of transaction fees.

Tradition barriers occur when innovation uncomfortably changes users' existing routines, while usage barriers refers to resistance towards the use of mobile payments due to factors such as inconvenience and the processing speed of mobile payments.

Value barriers refers to monetary value where consumers are reluctant to change the way they perform their task, unless the innovation offers a cheaper price compared to its substitutes.

For hawkers, when the return on investment in mobile payments is still unclear, the initial investment also imposes a value barrier to their adoption.

READ: Lessons from San Jose and Stan Lee as Singapore’s Smart Nation efforts enter new phase, a commentary

THE BIGGEST BARRIERS

The SUSS student survey found that 69 per cent of the hawkers agreed that cost barriers are a concern to them. Thus, incentive programmes that lower the monetary costs of adoption will entice more to adopt mobile payments.

In terms of tradition barriers, nearly 60 per cent of the respondents said they preferred to use cash for transactions, but they would be more likely to adopt mobile payments if all other hawkers did it as well.

A higher percentage — 65.8 per cent — of them would be more likely to use mobile payment if customers requested so.

Hawkers had mixed responses when it came to user barriers. About one third found that mobile payments were easy to use, while 31.2 per cent were not familiar with making transactions using mobile devices, or were afraid of making mistakes when carrying out such transactions.

Many hawkers polled were aware of the benefits of mobile payments. More than half, or 55.7 per cent, said they were aware that they did not need to worry about giving change when using mobile payment, and 46.8 per cent of them said they were aware that they did not need to worry about going to the bank and deposit their earnings.

But only 4.6 per cent agreed that mobile payments allowed them to pay their suppliers online.

READ: Going cashless at hawker centres: Challenges and opportunities

Despite hawkers’ continued preference for cash, the survey also throws up one positive aspect: More than half, or 56.1 per cent, intend to use mobile payments in the future, and 48.1 per cent say they intend to use mobile payments as often as possible in the future.

About 34.2 per cent and 11.4 per cent of respondents said they would encourage customers and suppliers to use mobile payments, respectively.

The survey suggests that among the persistent barriers to adoption, cost barriers and value barriers deter hawkers the most from adopting mobile payment.

Since cost is a concern to them, ramping up promotion efforts to lower the costs of adopting mobile payments, such as offering incentives and discounts to both hawkers to put these in place and their customer to use these, might help. Hawkers are more likely to adopt these modes of payments when they see customers demanding for it.

Second, marketing and educational efforts could be more hawker-centric, highlighting to them the tangible benefits of using mobile payments.

Such efforts must also go up the value chain to reach out to their suppliers to foster adoption so that hawkers do not have to fork out cash for raw materials, and to consumers whose behaviour will set the agenda for hawkers’ adoption of cashless payments.

News that the introduction of DBS Bank’s PayLah! has spurred the adoption of mobile payments with mall merchants the main beneficiaries are a testament to this.

Finally, the process of using mobile payments should be simple, easy and should not confuse both consumers and business users, especially those like hawkers, who are not well versed on how these mobile payment platforms work. In this regard, NETS' appointment as the “master acquirer” to supply hawkers with systems to accept e-payments should help speed up adoption.

With their myriad offerings and reasonable prices, Singapore’s ubiquitous hawkers and hawker centres have long been an integral part of the nation’s dining landscape.

Getting them to embrace mobile payment may expedite the island’s digital transformation.

Dr Huong Ha is head of the business Programme at the School of Business, Singapore University of Social Sciences. Carey Lin is pursuing a business degree at the same school.