commentary Commentary

Commentary: Who’s buying private property after last year’s cooling measures?

Actually, there is some resilience in the demand for private property in Singapore among specific groups of buyers, says Senior Director and Head, Knight Frank Research Dr Lee Nai Jia.

File photo of a condominium showroom from 2018. (File photo: TODAY/Nuria Ling)

SINGAPORE: Since the last property cooling measures rolled out in July 2018, market sentiments have remained subdued.

The new measures have led to higher acquisition costs for buyers and curbed their ability to take out larger loans to purchase private property, so from a theoretical standpoint, one would expect demand to decline together with prices.

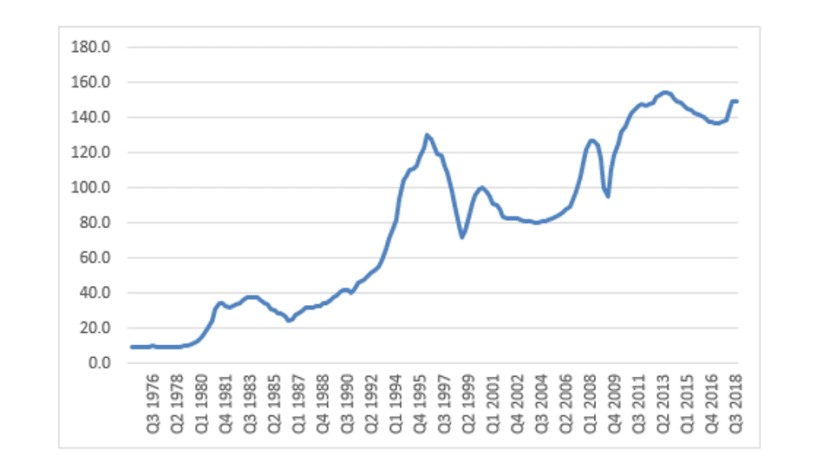

However, the impact on price remains to be seen. In the third quarter of 2018, the Residential Property Price Index (which include executive condominiums) continued to increase albeit at a slower pace. Singapore’s private home segment in 2018 rose nearly 8 per cent, compared with 1.1 per cent growth the year before.

SALES POST-COOLING MEASURES MIXED

Residential sales post-cooling measures have been mixed. In 2018, sales plunged by 55.2 per cent year-on-year in August, and 22.4 per cent year-on-year in October.

But in September and November, we saw an uptick of 18.9 per cent and 50 per cent year-on-year, respectively. The boost in demand in the latter months, however, can be attributed to new project launches with attractive locations and affordable price points.

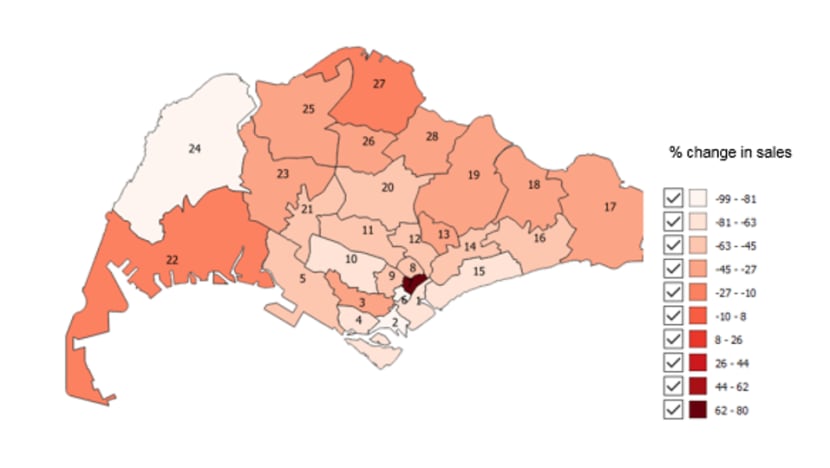

Overall, total sales volume for the private property market in 2018 was dragged down by a subdued resale market, tempered significantly post-cooling measures. The prime districts (of 9, 10, 11, 1, 2 and 4) and District 5 (Pasir Panjang, Hong Leong Garden, Clementi New Town) witnessed a relatively large drop.

The only district that saw an increase in sales was District 7, likely due to the launch of South Beach Residences, which was delicensed after receiving its Certificate of Statutory Completion.

Receiving their Certificate of Statutory Completions meant that subsequent sales of the project are considered resales, and buyers of properties such as this found that more attractive as there is a finished product for viewing and the unit can be moved into immediately.

Additionally, delicensed projects can offer the option of deferred payment schemes and so may have further contributed to the increased sales.

Despite cautious sentiments, sales picked up in November 2018 – developers sold 1,198 units, higher than the 788 units sold the same month in 2017, according to the Urban Redevelopment Authority (URA). The strong sales in November is significant as market activities historically tend to slow down with the year-end festivities.

The strong sales reflects Singaporeans’ persistently strong demand for private housing, not just as an asset for investment, but as a home for the future. Private housing continues to hold great appeal for upgraders with their modern amenities, as well as the societal status associated with owning a private property.

KEY GROUPS OF BUYERS

In 2019, we expect HDB upgraders to remain a key group of buyers driving private housing demand. The confluence of fewer interest rate hikes, stable private residential prices and the uncertain impact of the Voluntary Early Redevelopment Scheme (VERS) on HDB flats with expiring leases is likely to encourage more HDB flat owners to upgrade.

READ: Mind the varied impact of HDB schemes on different groups of home owners, a commentary

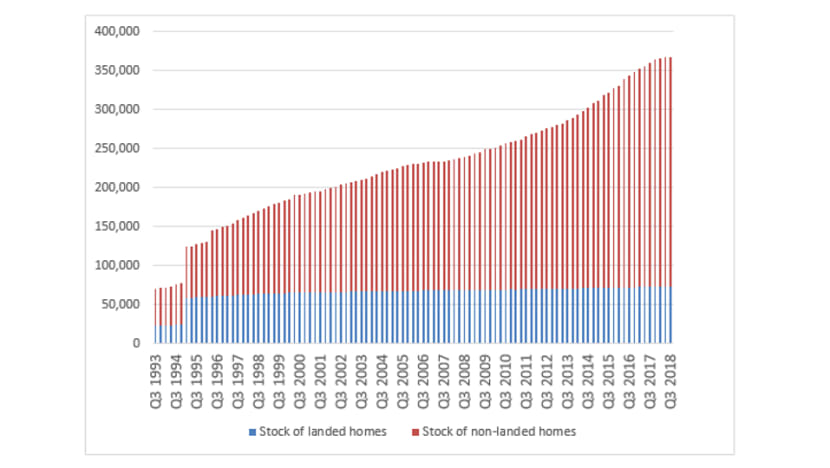

Separately, while non-landed homes in Singapore remain popular, the market for landed homes is expected to do well, as investors are attracted to this asset class due to limited supply.

According to URA, the total stock of landed homes grew by 7 per cent in the past decade, since the third quarter of 2008.

There have also been signs indicating that foreign buyers are slowly returning to Singapore’s residential market, from September 2018.

In August, foreign buyer purchases rose to 65 units in September, from 50 units in August 2018. The number of units purchased by foreigners then stayed largely unchanged, till November.

While the high Additional Buyer's Stamp Duty (ABSD) may continue to deter foreign buyers to a degree, prices of Singapore residential properties are likely to remain resilient compared to other assets, and continue attracting foreign high net-worth individuals seeking portfolio diversification or wealth preservation.

SINGLES AND SILVER POPULATION MAY ALSO MOVE TO PRIVATE HOUSING?

We should also expect a greater demand for smaller-sized private housing in 2019, from the rising number of singles among Singaporean citizens.

According to the annual Population in Brief report by the Department of Statistics, the proportion of single women aged between 25 and 29 rose from 60.9 per cent in 2007 to 68.1 per cent in 2017.

Among men, the proportion of the same age who stayed single increased from 77.5 per cent to 80.7 per cent, over the same period.

READ: The Lease Buyback scheme can give singles more housing options, a commentary

Separately, ageing baby boomers (born between 1946 and 1964), particularly those who have accumulated sufficient wealth, are also expected to contribute to the demand for smaller-sized housing in 2019, through right sizing.

As at 2016, data from population.sg estimates that approximately 1 million Singaporean citizens fit this profile. Correspondingly, this may give rise to demand for two-bedroom units, with right-sizing likely to occur in both private and public housing.

GROWTH AREAS WOULD CONTINUE TO ATTRACT BUYERS

Moving forward, we expect demand for private homes to remain exuberant, albeit tempered by the government’s new cooling measures, as buyers continue to be attracted to new neighbourhoods in Singapore.

For instance, despite the implementation of the Total Debt Servicing Ratio in 2013, demand for private residential properties in Jurong East and the Lakeside District surged, as buyers’ interests were spurred by the government plans to develop the area into the second Central Business District.

In the coming years, the next neighbourhood likely to generate huge buyer interest is the Punggol Digital district, which is expected to bring about 28,000 jobs to the Northeast region. As such, prices in the North East region are likely to resist pressure from a slowing market.

Furthermore, sales of executive condominiums are also expected to do well this year. Targeted buyers in this category have not been as affected by cooling measures, and prices for these projects are likely to remain affordable, compared to private projects.

The projects at Sumang Walk and Anchorvale Crescent will be popular among buyers, given the upcoming Punggol Digital District.

Unfortunately for some, interest rates are projected to increase in 2019, but this is unlikely to cause much direct impact on demand. The necessary upfront costs, down payment and ABSD however, will remain the bigger deterrent to purchasing private homes for equity constrained households.

Dr Lee Nai Jia is Senior Director and Head of Research at Knight Frank Singapore.