Malaysia’s restructured national pension fund allows for early withdrawals; experts say ‘delicate’ balance needed

Under the newly restructured plan, Employees Provident Fund (EPF) members now have three accounts compared with the previous two, with a new “flexible” one where funds can be easily withdrawn to meet short-term needs.

This audio is generated by an AI tool.

KUALA LUMPUR: For security guard Hassan Ahmad, a gross monthly salary of about RM2,000 (US$420) is not enough to sustain the expenses for his family of three.

After paying off his commitments that include the monthly rent, motorcycle payment and various other bills, the 28-year-old is left with about RM500 to last him for the rest of the month.

“It isn’t easy at all and I have to keep on borrowing money from my family members at times just to survive and buy rice,” said Mr Hassan, who lives in the nation’s capital, Kuala Lumpur.

The father to a three-year-old boy, therefore, is appreciative of the decision by the Employees Provident Fund (EPF) - Malaysia’s retirement fund - to allow its members to withdraw money from there to fund their short-term financial needs after a restructuring plan that took effect from May 11.

“I’m not sure if it will really be enough, but it is something,” said Mr Hassan, who is his family’s sole breadwinner.

Previously, EPF members who had not reached the age of 55 could only make withdrawals for healthcare, housing, and education purposes among others.

But now, members can make withdrawals at any time after the introduction of a new “flexible” account.

“The main focus of the EPF Account Restructuring initiative is to empower members in making decisions to balance future needs for retirement between short-, medium- and long-term financial needs,” EPF chief executive officer Ahmad Zulqarnain Onn said in a statement on Apr 25.

He added: “This initiative is not just EPF’s response to current needs, but is a proactive step to help members facing the changing job landscape and demographics of the population as well as the life cycle needs of EPF members.

"With these enhancements, the EPF strives to ensure that every EPF member can manage their finances with confidence and resilience in this dynamic and challenging environment.”

Reactions to the move to allow members to easily withdraw part of their retirement funds have been mixed, with some experts cautioning that the move may exacerbate a retirement crisis in the future.

“CROWD-PLEASING POLITICAL OBJECTIVE”

Under the newly restructured plan, EPF members now have three accounts compared with the previous two.

Seventy-five per cent of an individual’s monthly contribution will now go into Account 1, 15 per cent into Account 2 and the remaining 10 per cent will go into Account 3 - the new flexible account.

Previously, 70 per cent of the contributions were deposited into Account 1 and 30 per cent into Account 2. The money in Account 1 cannot be withdrawn until a member reaches the age of 55 while funds from Account 2 can be withdrawn for purposes such as housing.

Senior fellow with the Singapore Institute of International Affairs Oh Ei Sun told CNA that there appears to be two objectives to the move by EPF: One, which is to increase contributions into Account 1 and the other, to give members some flexibility in how they choose to utilise their funds.

Dr Oh said that the increase in allocation of funds to Account 1 enables EPF to “lock up” an extra five per cent for the long term, hence increasing its cash reserve and liquidity.

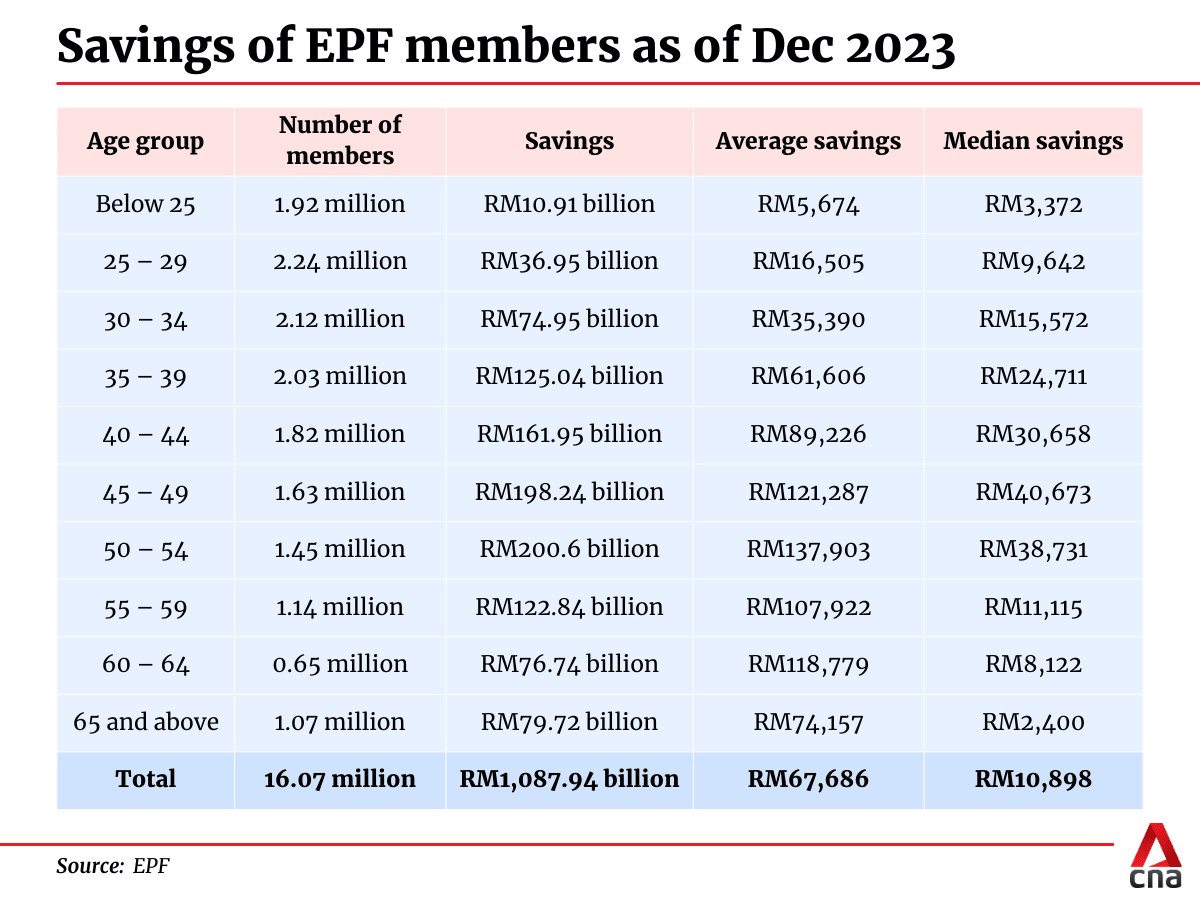

As of December last year, EPF had 16.07 million members, of which 8.52 million are active members. This represents 50 per cent of Malaysia’s 17.03 million labour force as at the end of 2023.

The EPF - one of the world’s largest retirement funds – has assets worth RM1.135 trillion.

“(The change) serves two objectives at the same time. The first is a financial objective benefitting EPF but the second is a crowd-pleasing political objective,” said Dr Oh, referring to the move to allow members flexibility in using their EPF deposits.

He believes that the move was partly motivated by the pressure from the opposition coalition to allow further withdrawals from the EPF.

Between 2020 and 2022, through four rounds of COVID-19 withdrawals, 8.1 million Malaysians took RM145 billion out of the retirement fund. The withdrawals were first approved when the country was led by then prime-minister Muhyiddin Yassin and continued under the leadership of Mr Ismail Sabri Yaakob.

Muhyiddin is currently the chairman of the opposition coalition Perikatan Nasional, which counts Islamist party Parti Islam Se-Malaysia (PAS) as well as Malay nationalist party Parti Pribumi Bersatu Malaysia (Bersatu) as among its members.

After the 15th general election in Nov 2022, Muhyiddin had urged the government to allow another round of EPF withdrawals for those in need.

However, Prime Minister Anwar Ibrahim had said in May last year that even though it was not a popular decision, contributors' savings must be protected so that they will have money for future use.

"Even though there is much political pressure to approve another round of withdrawals, I stand firm on my decision as EPF is a legal body which is there to protect contributors' money now and for future," he was quoted as saying by the News Straits Times.

Later during the tabling of the 2024 Budget in October, Mr Anwar appeared to have backtracked from his earlier position to announce that the government would be introducing a flexible EPF account that allows contributors to access the funds inside at any time.

PRESSURE FOR CURRENT NEEDS TO BE MET

Economists whom CNA spoke to said that while there may be political pressure that led to the move, there was a real pressing need for Malaysians to have access to the funds as they deem fit.

Bank Islam chief economist Mohd Afzanizam Abdul Rashid said there is a delicate balancing act between meeting the needs for retirement and at the same time, ensuring that members have sufficient cash to meet their personal needs especially for emergency purposes.

“There have been studies that suggest Malaysians would have difficulties to come up with an emergency fund when they really need it,” he told CNA.

Last year Bank Negara Malaysia governor Abdul Rasheed Ghaffour was reported to have said that nearly half of Malaysians have difficulties in setting aside RM1,000 for emergencies.

“So the move by EPF to allow such flexibility is for the members to navigate economic challenges brought by the higher cost of living which affects their purchasing power,” said Mr Afzanizam.

Meanwhile, executive director of the Socio-Economic Research Centre (SERC) Lee Heng Guie told CNA that the flexible account would come in handy when the government eventually implements its planned subsidy rationalisation programme.

The Anwar government has spoken about plans to shift away from blanket subsidies to a targeted system that mainly aids low-income groups, and this includes floating the prices of fuel in Malaysia.

“There is likely to be an impact and inflation is expected (to rise), especially more so when the civil servants receive a salary adjustment in December. It might come in handy for some people for some relief although it is best not to tap it,” said Mr Lee.

The economist also believed that the government made this decision to attract those who do not have any social protection such as gig workers to contribute to the EPF voluntarily.

Driver Hasbullah Mahmud, 50, told CNA that the flexible third account would be beneficial to those who urgently needed the money.

He had made several withdrawals from the EPF during the COVID-19 pandemic, but only did so because he was jobless at the time.

Mr Hasbullah, who hails from Klang, said that he would only make withdrawals if there was an urgent need to do so.

“Some of my friends have said that they want to take out the money, even though they have no real need to do so. I believe that the (untouched) money (left in the account) will be needed during our old age,” he said.

Legal counsel Syazwan Basri, 35, similarly told CNA that the flexible account was a good idea for those who needed to tap on the funds urgently.

Mr Syazwan said that he will try not to make any withdrawals from his EPF, and would opt to use his savings first even for matters such as housing.

He has decided not to transfer any money into his flexible account, believing that he does not have enough surplus to do so.

From May 12 to Aug 31, members are allowed to make a one-time transfer from their other EPF accounts to the flexible one to top it up. The amount allowed to be moved is based on a percentage as determined by the EPF.

On Monday, it was reported by Bernama that EPF offices all over the country were crowded with people who were trying to get more information about the flexible account.

“SHORT-TERM POPULIST POLICIES”

Meanwhile, there are others who are not in favour of allowing people to make early withdrawals from their retirement fund.

Former Bank Negara deputy governor Sukhduwe Singh for one had claimed that the move was based on politics and not economics.

“Of course, you can always pull some economists out of the woodwork to try to justify it. But the fact remains that a fund to support current consumption is fundamentally inconsistent with the mandate of EPF as a retirement fund.

“The precedent established by this proposal does not align with the long-term interests of EPF, its contributors, or Malaysia. We must not allow short-term populist policies to override the long-term interests of our country,” he had said in a Linkedin post on Apr 19 of this year, before the plan was announced.

The EPF has set RM240,000 as the basic savings target for contributors when they retire at the age of 55, although many believe that the benchmark is no longer feasible given the sharp rise in the cost of living.

As of Dec of last year, EPF’s 1.45 million members aged between 50 and 54 had only an average savings of RM137,903 in their accounts.

Mr Afzanizam of Bank Islam said the continuous early withdrawals might have an impact as EPF members would miss out the benefit of the compounding factor.

“The longer you keep the money in EPF, the larger the funds would accumulate due to the compounding factor,” he said.

Social Protection Contributors’ Advisory Association Malaysia (SPCAAM) labour advisor Callistus Anthony D’Angelus said in a statement on Apr 27 that such a mechanism has been instituted because a good number of contributors cannot survive economically based on their income levels.

“Wage levels have been depressed for decades, and it is done knowingly through an unholy alliance between big business and the government. By the government, I mean the different administrations that have been in place and it includes the current coalition government,” he said.

Malaysia has a minimum wage level of RM1,500.

“Where workers, the B40 and M40 communities are concerned, there has been no reform which has benefited them. It is unfortunate as the coalition government has failed to introduce reform to deal with the acute cost of living crisis afflicting the poor,” he added.

The managing director of research firm DM Analytics Muhammed Abdul Khalid told CNA that the “ideal path” forward would be to not allow any early withdrawals but acknowledged that the flexible account was a way to mitigate demands made by the public following the four withdrawals allowed by the previous administrations during the COVID-19 pandemic.

“What I personally like about this is that while you can withdraw from Account 3 if you choose to, there is a 5 per cent increase for your Account 1. So your forced savings has increased. This is a positive,” he said.

He, however, does not believe that it is enough to help the lower income group, many of whom work in the informal sectors.

“Not all workers have EPF, about 40 to 50 per cent … Even if you have EPF, those who are from the lower income groups have cleaned up their accounts during the four (earlier) withdrawals. What is needed is higher wages,” he said.

Meanwhile in Singapore, several changes were made to the Central Provident Fund (CPF) - set to take place from 2025 - in order to better support the retirement needs of seniors in the country, it was previously reported.

Members aged at least 55 will no longer have a Special Account from 2025 onwards, but they will be able to put more money into their Retirement Accounts. Having more money in a CPF Retirement Account translates to bigger monthly payouts.

Further, CPF contribution rates for those aged 55 to 65 will be increased by a further 1.5 percentage point next year.

According to the CPF website, members can generally withdraw at least S$5,000 or any amount in excess after setting aside their Full Retirement Sum when they turn 55.

CPF members will also be eligible to start receiving their monthly payouts from the age of 65. They have an option to start the payout anytime from 65 to 70 years old.

MORE IS MORE

Meanwhile, there continues to be those who are still unhappy with the recent changes to Malaysia’s EPF scheme, with the Pertubuhan Gagasan Inovasi Rakyat Malaysia (PGRIM) for one insisting that the government allow withdrawals to be made from Account 1, instead of only the flexible account.

Its president Azmie Mohd Tahir wrote in a petition on May 2 that flexibility was needed to allow some EPF members to transfer money from Account 1 into the flexible account.

“The burden of the high cost of living is increasing and many people out there are under more pressure and becoming desperate,” he said.

A social media user by the name of Ilham commented on the group’s Facebook page that while he was grateful with the EPF decision, most of those in the lower income (B40) group had very little money in their EPF accounts.

“The EPF does not understand the plight of all its contributors. Many of them don’t have any money in their Account 2 and are the most affected. They are the ones that need to pay off their debts and survive. If the government allows money to be transferred from Account 1, many contributors can benefit,” he said.

But for legal counsel Syazwan, he told CNA that he is taking a more cautious approach to his retirement funds.

“I want to be careful and I will try not to touch my EPF money because it is for retirement,” Mr Syazwan said, adding that if EPF members can get up to RM1 million in their account by the time they retire, they could even live on the dividends given by the retirement fund alone.