PRESENTED BY

SECURE A LIFETIME OF COVERAGE

Content share and bookmark

SECURE A LIFETIME OF COVERAGE

Even though people are generally healthier, there is still a possibility that severe disability may arise in late adulthood. It is understandably difficult to accept that as we age, our health will decline, and we will inevitably experience some limitations in everyday functioning. However, planning ahead can make a big difference in how individuals and their families navigate a disabling disease in the future.

CareShield Life, a national long-term care insurance scheme, offers the protection and peace of mind many are seeking. It provides Singaporeans with basic financial support should they develop severe disability, especially during old age, and need personal and medical care for a prolonged duration.

WHY PLANNING FOR LONG-TERM CARE MATTERS

Government statistics reveal just how rapidly Singapore’s population has aged over the past decade. The proportion of citizens aged 65 and above increased from 11.1 per cent in 2012 to 18.4 per cent in 2022. By 2030, seniors will make up nearly one in four (23.8 per cent) of the population.

Against this backdrop, the age-related disease burden is expected to rise in the coming years. According to the Ministry of Health (MOH), one in two healthy Singaporeans aged 65 could develop severe disability in their lifetime and require long-term care. Severe disability in this context is defined as being unable to perform three or more activities of daily living (i.e., washing, toileting, dressing, feeding, walking or moving around, and transferring from bed to chair and vice versa).

There are several ways a person could develop severe disability later in life. For example, ageing is the biggest risk factor for dementia, a chronic and progressive disease that causes deterioration in cognitive function. Individuals with worsening diabetes, a common chronic disease which MOH has declared a war on, are also at risk of severe disability. If poorly controlled, diabetes can lead to blindness, kidney failure, limb amputation and other complications. Then there is the possibility of a sudden disabling event such as a stroke or spinal cord injury, which may happen when one least expects it.

Whether an older adult suffers a sudden stroke or has a chronic illness that worsens over time, the outcome is often the same — severe disability, which in turn is associated with high long-term care costs. The cost varies widely, based on an individual’s condition, type of disability and care preferences. As a rough gauge, it could range between S$900 and S$4,000 per month before subsidies, depending on whether care is provided at home, at a day care centre or in a nursing home. Add up the monthly expenses over an extended period, and it is easy to see why some families may struggle to afford such care.

It is this very group that CareShield Life aims to help. The insurance scheme provides basic financial protection against the potentially high costs of long-term care, thus easing the strain on individuals and their families.

ELDERSHIELD VS CARESHIELD LIFE: AN UPGRADE IN BENEFITS

Launched in October 2020, CareShield Life is an enhanced version of ElderShield. There are several key differences between the two schemes, with CareShield Life providing better protection than ElderShield through higher and lifetime payouts.

CareShield Life has been gradually rolled out nationwide since its launch, beginning with younger people. Singapore Citizens and Permanent Residents (PRs) born in 1980 or later are automatically covered under CareShield Life from October 1, 2020, or when they turn 30, whichever is later, regardless of any pre-existing severe disabilities.

Older cohorts have subsequently come on board the scheme. On December 1, 2021, Singapore Citizens and PRs born between 1970 and 1979, who were insured under ElderShield 400, and who did not have severe disability — that is, able to perform three or more activities of daily living — were automatically enrolled into CareShield Life.

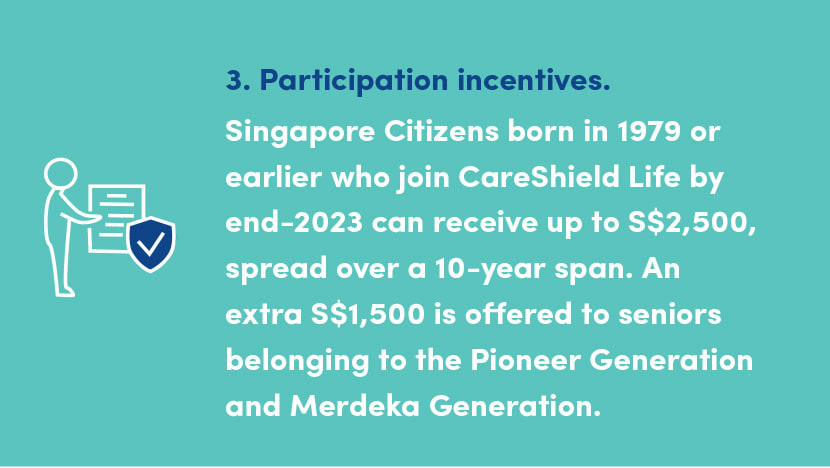

Currently, participation in CareShield Life is optional for the rest of the population. Singapore Citizens and PRs born in 1979 or earlier who were not auto-enrolled are invited to join, as long as they do not have severe disability. To encourage sign-ups, those who apply before the end of this year can receive participation incentives of up to S$4,000.

HOW TO MAKE PREMIUM PAYMENTS

Compared to ElderShield, policyholders of CareShield Life pay higher premiums annually until age 67 or for 10 years (whichever is longer). However, the fact that CareShield Life offers higher and lifetime payouts more than makes up for the increased premiums.

Moreover, a range of financial support measures is available to help offset CareShield Life premiums and ensure they remain affordable. For example, annual premiums can be fully paid using the policyholder’s MediSave — which, in the case of seniors, is topped up each year as part of the Pioneer Generation Package and Merdeka Generation Package — or that of their family members. Eligible individuals may also qualify for means-tested government subsidies, participation incentives and Additional Premium Support.

Life is unpredictable and full of twists and turns. That said, getting insured helps take the sting out of uncertainty. Making preparations to alleviate the costs of long-term care in the event of severe disability offers greater peace of mind, not just for oneself but for one’s family members too.

In the stories that follow, three individuals — including a caregiver, a retiree and a working adult — share their personal experiences and motivations for joining CareShield Life. Although their circumstances differ, each expresses a sense of optimism about the future in knowing their long-term care needs (or those of their loved ones) are covered should the unexpected happen.

Read their stories, and consider signing up too.