CapitaLand shares jump 20% on restructuring plans; analysts say proposal ‘highly value-unlocking’

A man walks past real estate developer CapitaLand's logo. (Photo: AFP/Theresa Baraclough)

SINGAPORE: Shares of CapitaLand jumped as much as 20 per cent on Tuesday (Mar 23), a day after the real estate behemoth announced a major restructuring plan to consolidate its fund management and lodging business into a new entity, and take its property development business private.

Market analysts were generally positive on the company's proposed restructuring, with one describing it as “highly value-unlocking”.

READ: CapitaLand to separate real estate development and fund management units

The counter, which resumed trading on Tuesday after a one-day trading halt pending its announcement, surged more than 20 per cent, or S$0.68, to S$3.99 per cent at the open.

It trimmed gains throughout the day and ended 13.3 per cent higher at S$3.75. More than 88 million shares exchanged hands, making it one of the most heavily traded securities by volume.

The broader Straits Times Index edged up 0.1 per cent to finish at 3,131.74.

ONE BECOMES TWO

The restructuring plans come after CapitaLand posted its first annual loss in nearly two decades last year due to the COVID-19 pandemic.

The proposal to split itself into two is meant to sharpen the group's focus on strategic growth and create shareholder value, the company said.

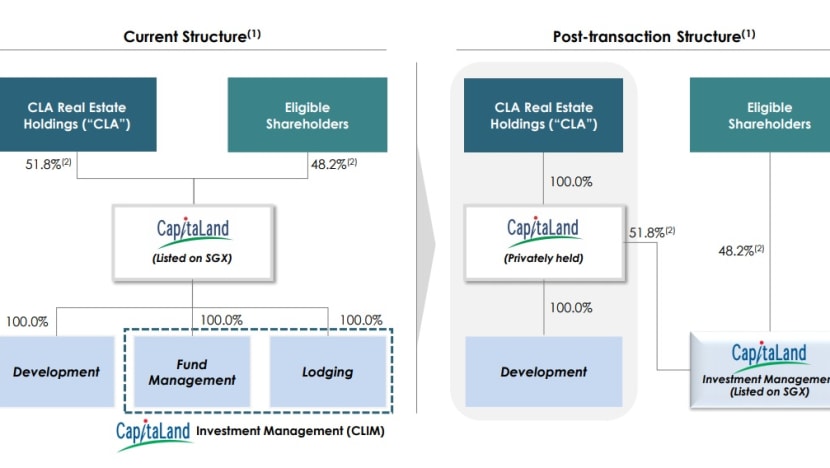

The first entity, called CapitaLand Investment Management (CLIM), will house its stakes in its real estate investment trusts and business trusts, selected unlisted funds it is currently managing as well as its lodging business.

Set to be listed on the Singapore Exchange, CLIM is expected to be Asia’s largest real estate investment manager with assets under management of about S$115 billion.

It will be asset-light and capital efficient, as well as focusing on growth in fee income and funds under management, the company said.

Meanwhile, its real estate development business will be taken private and become part of CLA Real Estate Holdings, its largest shareholder. CLA is an indirect wholly owned unit of Temasek Holdings.

Being capital intensive and requiring longer gestation periods, this side of the business may “not (be) adequately appreciated by the public markets”, said CapitaLand group chief executive officer Lee Chee Koon in a news release announcing the plans on Monday.

“With a privately held development business, we will be able to better ride property development cycles to optimise returns across asset classes and geographies,” he added, noting that the privatised development entity will continue to develop projects as a key source of pipeline for CLIM.

Overall, the move to split into “two distinct entities” will fit into the company’s longer-term objective of becoming a “globally competitive real estate developer and asset manager”. It will also give the company flexibility to be able to “match the right level of capital to the business objectives”, said Mr Lee at a media and analyst briefing on Monday.

Under the deal, shareholders will receive an implied consideration of S$4.102 per share in cash and scrip, including a one-for-one equivalent stake in CLIM.

That is 24 per cent above the last traded price of CapitaLand and represents a premium of 27 per cent to the one-month volume-weighted average price.

“HIGHLY VALUE-UNLOCKING”

Monday’s announcement was “a bit of a surprise” considering how CapitaLand has done a few major deals over the past two years, RHB analyst Vijay Natarajan told CNA.

These include the S$11 billion cash-and-stock deal to acquire Temasek's shares in Ascendas-Singbridge in 2019, and last year’s merger of CapitaLand Mall Trust and CapitaLand Commercial Trust.

“The pace at which CapitaLand has been restructuring to deliver shareholder value and reposition its business has been much faster than we expected,” said Mr Natarajan, adding that the pandemic and an increased focus on “new economy” assets by the company could have been catalysts for the latest move.

Mr Natarajan noted that there “is merit” in the proposed restructuring. For CapitaLand shareholders, it would mean retaining exposure to a fast-growing fund-management and fee-income business, and allow them to participate in future upside potential.

This is less risky than the development arm, whose margins across markets have also been under pressure due to cooling measures and rising construction costs.

“CapitaLand’s move to strategically restructure its portfolio by privatising its development arm and maintaining the listing of its investment management arm is a highly value-unlocking move,” he wrote in a research note.

The implied offer price per share is "fair" given current market conditions, he added. "We recommend unitholders to vote in favour."

Echoing that, OCBC Investment Research, which was “generally positive” on the proposed restructuring, noted that CLIM would generate more recurring income streams and fetch a higher valuation than the traditional property development business.

The new entity would also be less susceptible to property cooling measures, which tend to be more targeted at the residential sector, the team added in its research note.

That said, some questions remain.

For instance, Mr Natarajan said he would look at the company’s management structure following the restructuring, and how CapitaLand ensures a smooth transition.

The analyst is also seeking more clarity on how CapitaLand classifies and looks at acquisition assets across various business entities post-restructuring, as “there may be some overlap of interests”.