commentary Commentary

Commentary: Concerned about what fall in private home sales mean? Market fundamentals paint a different story

A holistic approach that considers affordability and financial planning, coupled with a long-term view are crucial when investing in property, says Ismail Gafoor.

File photo of a private condominium in Singapore. (Photo: Eileen Poh)

SINGAPORE: Property news headlines these days have left many scratching their heads.

Sales have been hitting multi-year highs in one month, but plunging the next – all this amid the deepest recession in Singapore due to the ongoing pandemic.

Last October, new private home sales fell by 51.7 per cent to 642 units, down from September’s two-year high of 1,329 units, leading some to wonder if pent-up demand has started to fizzle out.

Others questioned if this was a result of new restrictions on the re-issuance of Options to Purchase (OTPs) implemented at the end of September.

LISTEN: The Singapore property market: Is it changing for good?

But monthly sales figures do not fully reflect the state of the overall market and buying behaviour of consumers.

Potential buyers and sellers evaluating the private residential market should focus on market fundamentals, including demand and supply dynamics, price trends, and historical data and adopt a holistic approach and take a long-term view when investing in property.

READ: Property experts weigh in on removal of some pricing data from URA portal

DEMAND FIZZLING OUT?

Property news that make headlines are sure to garner attention. The October decline in private home sales was little different.

While the new OTP rule may have had some impact, the main reason for October’s sales drop was more likely the simple lack of launches during the month. There was only one new project in October – Hyll on Holland, which sold five units.

In contrast, September’s sales were boosted by launches such as Penrose, Verdale and Myra which contributed to nearly 34 per cent (or 448 units) of the monthly sales. Without these new launches, September’s sales would not be that much higher than October.

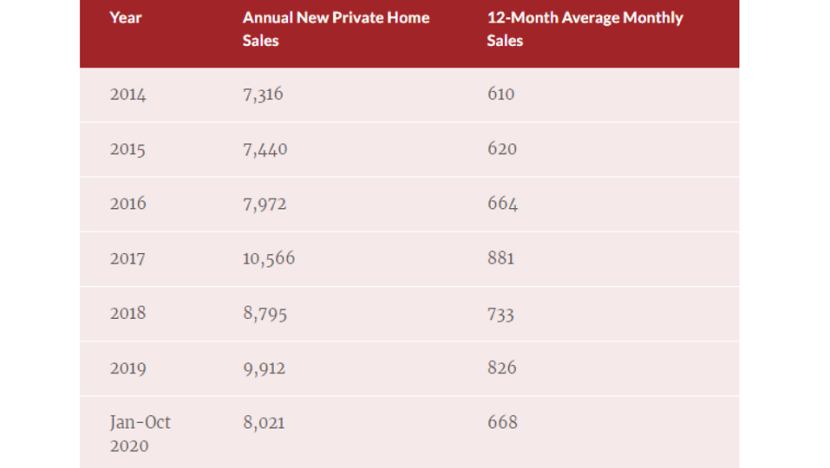

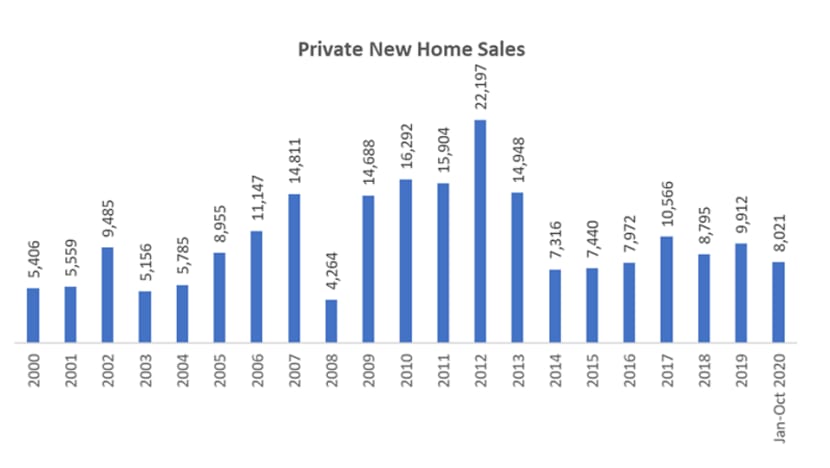

Developers’ monthly sales crossed 1,000 units from July to September before falling in October. Looking at the final two months of 2020, new home sales are not likely to breach the 1,000-unit mark, given limited mega launches ahead.

It is also worth noting that average monthly new home sales have not exceeded 1,000 units since the introduction of new cooling measures in June 2013.

But underlying demand for private homes has been strong throughout the pandemic, driven by local buyers and HDB upgraders.

Home sales rebounded in the second quarter of 2020, after the end of the circuit breaker imposed from Apr 7 to Jun 1. Of note, about 80 per cent of new private homes sold in the first nine months of 2020 were bought by Singaporeans – representing the highest proportion since 2010, according to Realis data.

During the circuit breaker, consumers became more comfortable with digital property marketing and virtual viewings. They also probably had more time to evaluate their real estate portfolio and investment plans.

Knowing that the market has turned in favour of buyers – coupled with the low interest rate environment and ample liquidity in the market – many consumers with ready funds made their property purchases between July and September.

READ: Commentary: How much should young couples spend on their first home?

PROPERTY MARKET ON FIRMER FOOTING

That the property market remains resilient despite COVID-19 and Singapore’s worst recession on record did not happen by chance.

The series of cooling measures rolled out in previous years placed the property market on firmer footing, heading into this crisis. They led to limited speculative activity, households purchasing homes prudently and home prices moving more in line with economic and income growth.

The property market today is stable and should see sustainable growth. This was not the case in past crises where the property market seemed to go through a boom-bust cycle.

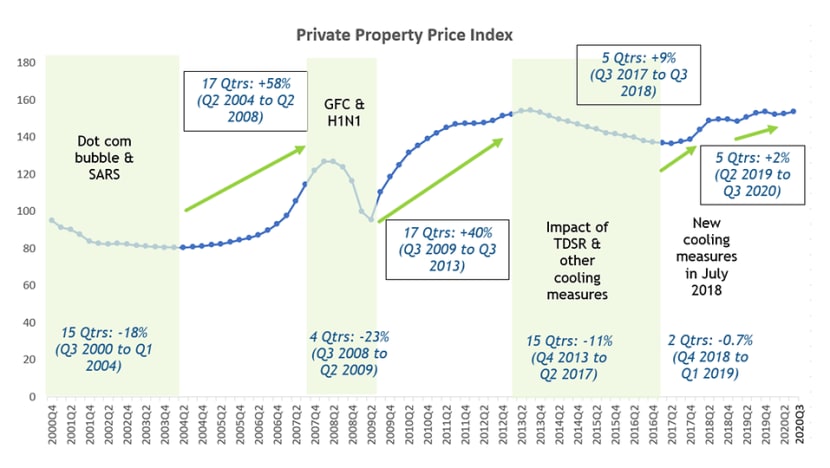

When the dot-com bubble burst in 2001, Singapore recorded a full-year GDP contraction of 1.1 per cent and the private property price index plunged 11.7 per cent that year.

In 2003, when SARS hit Singapore, private home prices posted a 2.1 per cent decline for the full year, before recovering in 2004.

What followed was 17 quarters of growth where prices increased by 58 per cent from Q2 2004 to Q2 2008.

READ: Commentary: Why Singapore's private residential market will remain attractive in the long term

The price growth ground to a halt following the global financial crisis, which saw home values fall by 23 per cent from Q3 2008 to Q2 2009.

Then came another wave of price increase over 17 quarters from the second half of 2009 to Q3 2013 where values jumped by 40 per cent. This was also the period where a flurry of cooling measures was introduced.

After the June 2013 measures were in place, property prices began to move in a more orderly manner. Following a couple of quarters of sharper price rise in 2018, fresh cooling measures were introduced in July 2018.

READ: Commentary: Who’s buying private property after last year’s cooling measures?

STABLE PRICES AND A RESILIENT MARKET

All in all, the Government – which has said it will continue to watch the market closely – has successfully engineered a soft landing in the property market, ensuring that prices do not run away from economic fundamentals.

The huge stimulus – almost S$100 billion – that the Government has committed as part of its COVID-19 response has also helped to save jobs and support the housing market.

This war chest is substantially bigger than the S$230 million SARS Relief Package announced in April 2003, and the S$20.5 billion Resilience Package put forth in January 2009 in the wake of the global financial crisis.

READ: Commentary: Winds in the Singapore economy sails are starting to stir

For home owners and investors, the various cooling measures – total debt servicing ratio, additional buyer’s stamp duty, seller’s stamp duty, lowered loan-to-value ratio – will help them make more prudent property buying decisions.

Being less leveraged on property purchase, households should have better holding power when the going gets tough, mitigating distressed sales.

These curbs have also helped to eliminate speculation in properties, leading to more stable prices and a more resilient market.

LISTEN: COVID-19 and the outlook for Singapore’s residential property market in 2020 and beyond

CONSIDERATIONS WHEN BUYING PROPERTY

Despite uncertainties ahead caused by the pandemic, the outlook for the property market remains positive over the mid- to long-term, because Singapore’s fundamentals – safety, political stability, a competitive and pro-business environment – are still intact.

In evaluating property investment, buyers should focus instead on two main areas: Affordability, and thorough financial planning to ensure they can hold on to the property for at least 5 years.

Ideally, buyers should have a financial safety net of 12 months’ worth of mortgage payment set aside (either in cash or in the CPF) to tide them through any unforeseen events, such as job loss.

READ: Commentary: Worried about keeping your job? Here’s advice to soothe your concerns no matter how old you are

Even if a buyer is purchasing a home for his or her own stay, it is still important to consider the property’s capital appreciation potential, in ensuring one’s retirement adequacy in the future.

A property purchase is a significant financial commitment. Buyers should be clear-headed about their financial ability, housing needs and investment objectives, and be less caught up with emotions roused by news headlines or the fear of missing out.

Ismail Gafoor is CEO of PropNex.

Listen to Ismail Gafoor discuss developments in the property market since COVID-19 hit on the Heart of the Matter podcast: