CNA Explains: What you need to know about changes to the Working Mother's Child Relief

The tax relief scheme has gone from being a percentage of income to a fixed sum, after Budget 2023.

(File photo: AFP/Peter Parks)

SINGAPORE: From 2025, the Working Mother’s Child Relief will change from a percentage of earned income to a fixed sum.

Announcing changes to the tax relief scheme during his Budget 2023 speech on Tuesday (Feb 14), Deputy Prime Minister Lawrence Wong said this would provide more Government support for eligible lower- to middle-income working mothers.

How does the Working Mother’s Child Relief work, and how will your tax reliefs be affected by the changes? Here’s what you need to know.

WHAT IS THE WORKING MOTHER’S CHILD RELIEF?

The Working Mother’s Child Relief is a tax relief scheme that aims to encourage women to continue working after they give birth to Singaporean children.

The amount of relief claimable is based on the child’s order in the family - determined not only by birth order, but the order in which the child joins the family.

The Working Mother’s Child Relief was first introduced in 2004 for the Year of Assessment 2005, applicable to parents of Singaporean children born from Jan 1, 2004.

This starting version of the scheme provided working mothers tax relief of 5 per cent, 15 per cent, 20 per cent and 25 per cent of their earned income for their first, second, third and fourth child respectively.

In 2008, these figures were increased to 15 per cent for the firstborn, 20 per cent for the second-born and 25 per cent for the third child and beyond.

The total amount of relief an eligible working mother can claim for all her children was capped at 100 per cent of her earned income for the Year of Assessment.

The relief was also subject to a total cap of S$50,000 per child, with claims under the Qualifying Child Relief and the Handicapped Child Relief counting towards this ceiling.

In 2016, the Ministry of Finance (MOF) implemented a S$80,000 cap on the amount of personal income tax relief an individual can claim, which took effect from the Year of Assessment 2018.

At the time, MOF estimated that 99 per cent of taxed residents would not be affected, and that about 90 per cent of women claiming the Working Mother’s Child Relief at the time were expected to be unaffected by the cap.

WHO CAN CLAIM THE TAX RELIEF?

According to the Inland Revenue Authority of Singapore’s (IRAS) website, working mothers who are married, divorced or widowed can claim the tax relief.

The child must be either born to the mother and her spouse or former spouse; a step-child; or legally adopted.

The child must also be below 16 years old or studying full-time at any university, college or other educational institute for the year that is assessed.

The child must not have an annual income exceeding S$4,000. This includes allowances and salaries from National Service, internships, school attachments and part-time jobs.

For example, a working mother who gave birth to a Singaporean child in 2016, adopted one in 2018 and gave birth to another in 2021 will be able to claim tax relief for all three of them. This will apply even if the adopted child is older than the other two children.

WHAT HAPPENS IF I HAVE CHILDREN BORN BEFORE JAN 1, 2024?

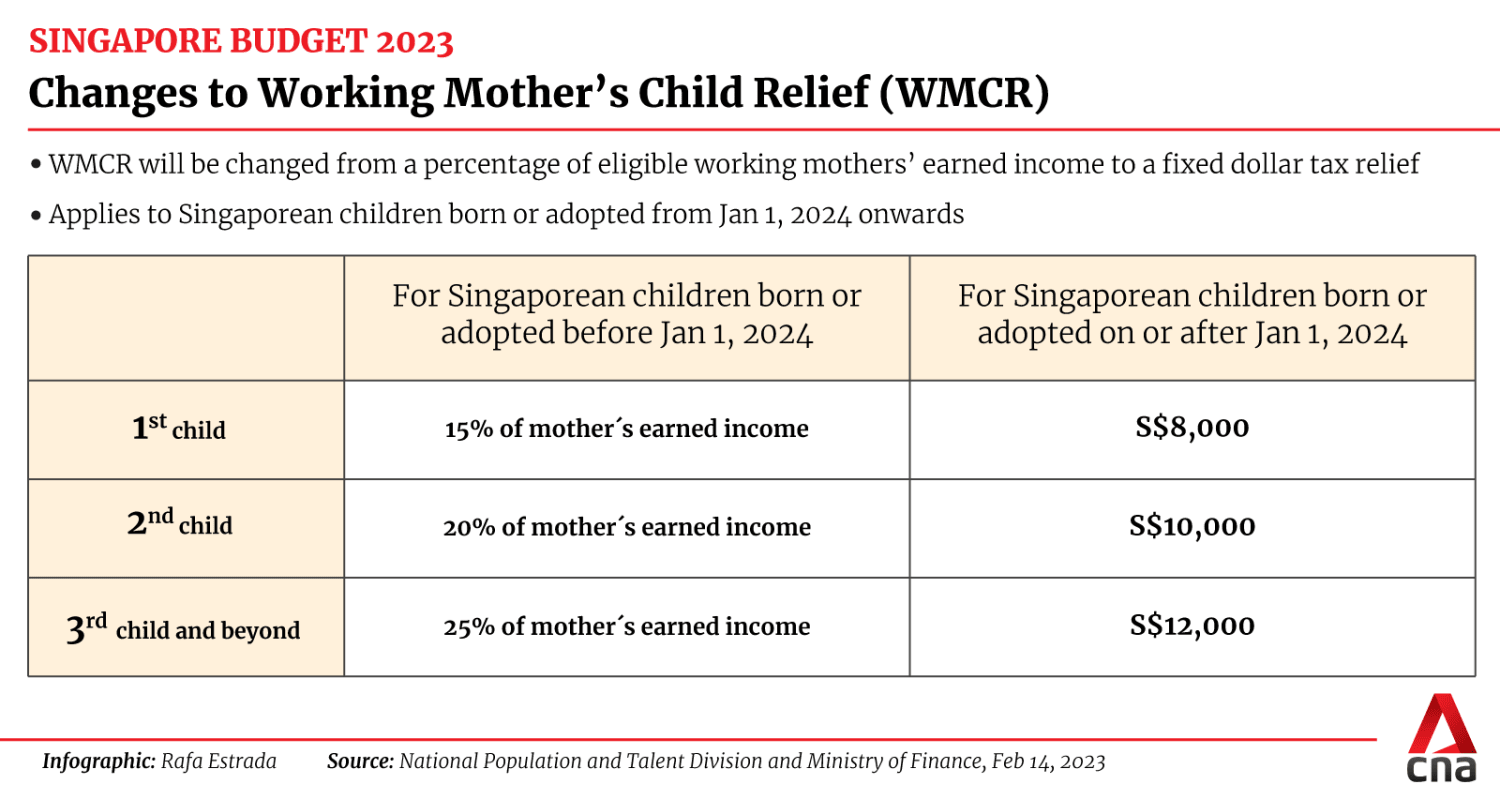

Under the changes announced by Mr Wong on Tuesday, eligible working mothers will now be able to claim S$8,000 in tax relief for their first child, S$10,000 for their second and S$12,000 each for their third and beyond.

But this will apply only to working mothers with Singaporean children born or adopted from Jan 1, 2024.

The changes will take effect from the Year of Assessment 2025, which would take into account earnings from 2024.

For working mothers with Singaporean children born or adopted before Jan 1, 2024, there will be no changes to their Working Mother’s Child Relief. They can continue to claim it based on the existing scheme.

For example, if a working mother has two Singaporean children born in 2021 and 2024, she will be able to claim tax relief of 15 per cent of her earned income for the first child - and S$10,000 for her second child, for the 2025 Year of Assessment.

DO THE CHANGES MAKE THE SCHEME MORE PROGRESSIVE?

In his Budget speech, Mr Wong said the measures were meant to support parents with the costs of raising their children.

He said the Government already has a “generous” set of measures, but some of these "need to be adjusted, to ensure that more support is given to those with greater needs”.

Under the Working Mother’s Child Relief's previous structure based on percentage, mothers who earned more income each year could claim a larger amount of tax relief for each child.

Take, for example, a working mother who earns S$100,000 per year and has one child born before 2024. She can claim S$15,000 in tax relief per year, bringing her chargeable income to S$85,000.

But for a working woman who earns S$100,000 per year and gives birth to her first child in 2024 or after, she can only claim S$8,000, bringing her chargeable income to S$92,000.

On the other hand, for a working mother who earns S$40,000 per year with one child born before 2024, S$6,000 can be claimed in tax relief per year. Her chargeable income will be S$34,000.

A working woman who earns the same and has her firstborn after 2024 can claim S$8,000 in tax relief per year. This will bring her chargeable income to S$32,000.