Family members and friends asking to borrow money? Don’t let guilt get to you

Choosing to lend money to someone is a deeply personal decision, but there are times when doing so will not help the borrower settle the root problem. It may even feed an addiction.

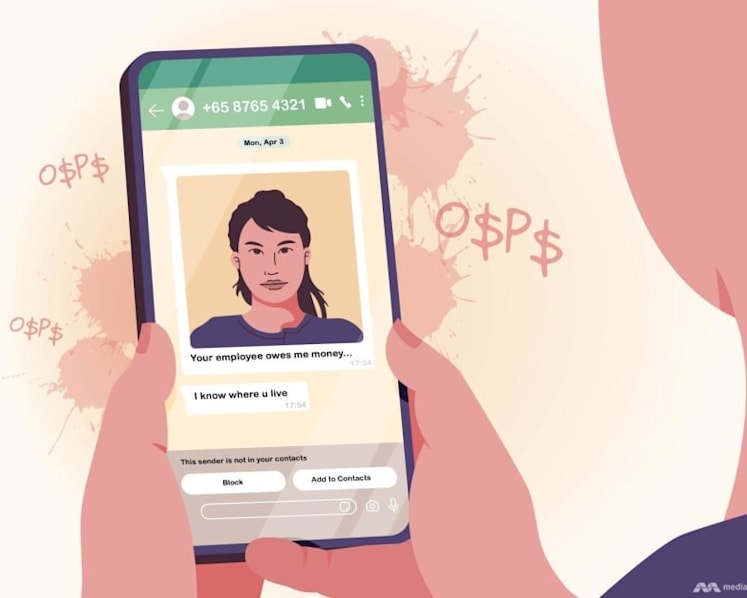

If you do not want to lend money to someone, it will be important to take time to explain your reasons, best done face-to-face, counsellors said. (Illustration: CNA/Samuel Woo)

This audio is generated by an AI tool.

Adulthood is not just one phase of life but comes in stages. Its many facets can be overwhelming, from managing finances and buying a home to achieving work-life balance and maintaining healthy relationships. In this series, CNA TODAY's journalists help readers deal with the many challenges of being an adult and learn something themselves in the process.

After entrepreneur Bertram Yang posted on his social media accounts that he had sold off the shares of his digital advertising firm, he started receiving messages from friends whom he had not talked to for years.

“These were National Service buddies and secondary school friends in particular," the 36-year-old said. "The conversations started cordially, but after a few texts, they would say, 'Bro, actually I’m in need of some money'.

“They asked for small amounts at first, so I would just transfer it. Then after that, it escalated. Some said they had a family emergency and asked for a few hundred dollars.”

He lent one of them S$220 and received S$150 back after reminding the friend several times. For the rest, they ghosted Mr Yang and he decided not to chase them for the sake of his own sanity, he added.

So what should you do if someone asked to borrow money from you, saying that it was urgent?

Counsellors said that choosing to lend money is a deeply personal decision that requires careful consideration of potential outcomes.

Friends or family members might ask for money due to a variety of reasons, including unexpected medical expenses, job losses, investment opportunities or to fund unhealthy addictions, the counsellors added.

Ms Tan Huey Min, general manager of Credit Counselling Singapore, said: "If the person wants money for urgent medical needs and if you have the money to spare, of course, you may want to help. But if the person says, 'I want to pay my credit card bills', then I think you should try to find out more."

Credit Counselling Singapore is a non-profit social service agency and the only organisation recognised by the Association of Banks in Singapore for its role in helping debt-distressed individuals through counselling, education and other programmes where suitable.

Psychotherapist Lilian Lee-Cutts from private clinic Counselling Perspective said that asking loved ones for money is a convenient way for borrowers to get the money they need while avoiding high interest rates from bank loans.

Mr Michael Chin, a freelance mental health counsellor, said: “Money is a sensitive topic that often causes strain in interpersonal relationships, especially when a borrower is unable to repay a loan on the agreed timeline. In these situations, it could put you in a difficult position and cause emotional distress.”

To lessen such distress, it may help to think of what it is like from the borrower's perspective.

If the person wants to borrow money because he has lost his job, has overdue bills and no savings, then it is logical to conclude that he would not be able to repay you in the short term until he finds a job and has had time to amass some savings.

Ms Tan said: "The person is in no position to pay you back – not that he doesn't want to, but he just cannot do so.

"Then, there are the borrowers in the other group, those who have no intention to pay you back at all. Even family and friends can 'vanish' or ghost you. Or even die before they repay you, if they have serious health problems and need to borrow money for medical bills."

For Mr Yang, he decided that it was not worth the stress and posted an Instagram Story stating that he would not entertain future requests for money. “I try to be more emotionally detached now,” he said.

He also blocked on messaging channel WhatsApp the friends who did not return the money they owed him, and he has chastised himself for being too “dumb and trusting”.

TO LEND OR NOT TO LEND?

Counsellors who spoke to CNA TODAY cautioned that lenders should take into account many factors before deciding to part with their money and they should find out why the borrower needs the money.

Most important of all, be prepared to never see the money again.

Ms Tan summed it up this way: "When you lend money, you must have the means to give.

"And if you want to lend money to anyone, whether the person is close to you or not, the best thing to do is to say goodbye to the money. When we expect people to pay us back, oftentimes, we will get disappointed. If you have the means and you are prepared to give the loan as a gift, you will have more peace."

Ms Lee-Cutts agreed, saying you must be prepared that the money “turns into a gift rather than a loan”.

She and Ms Tan also said that lenders must think about their own financial situations first.

"You have to take care of yourself first. If you don't have the means, think twice," Ms Tan said, adding that being a guarantor for someone is also not advisable.

"Guarantor means what? It means that when the borrower cannot pay back the loan, the guarantor is guaranteeing that he or she will pay back the lender on the borrower's behalf. So you also have to think carefully, because your own family and dependents will suffer as well if you are caught in a financial bind.

"It is hard to say 'no' to someone who wants to borrow money, but there are times you just have to do that when you consider the fuller picture," Ms Tan advised.

Psychologist Evonne Lek from Reconnect Psychology and Family Therapy said that another thing to consider is whether you want to risk losing a friendship if the borrower cannot repay the loan. Lenders might feel resentful from the experience, as Mr Yang did.

If the borrower is close to you, Ms Lee-Cutts suggested that you observe whether the person truly listens to you during face-to-face conversations and shows respect for your concerns.

You should also think carefully if the other party is asking for an inappropriately large amount of money, she added.

Mr Chin the counsellor advised people to look out for habitual borrowing patterns, vague reasons behind the requests, the absence of a repayment plan and emotional manipulation such as threatening self-harm or exerting pressure.

He emphasised that providing financial assistance to the borrower might not address the core issue and could worsen the problem.

“Giving money to people with a gambling addiction might enable destructive behaviour, further compromising their quality of life.”

However, the counsellors acknowledged that as close friends and family members to the borrower, lenders would want to show that they care about their loved ones. Refusing the other party might cause them to feel guilty about not helping those in need.

Ms Lek suggested that if you decide to lend money, you should spend some time discussing the nature of the loan and set clear expectations about repayment timelines.

This could be a written agreement that specifies a manageable monthly instalment amount.

She added: “When you say that you can only lend a fixed amount of money, they should respect that and not push for more.”

Mr Chin agreed that clear communication and mutual understanding can help maintain trust and minimise tension.

However, Ms Tan cautioned that when formalising a simple agreement of money owed and a repayment plan, it depends on how open-minded the two parties are and their level of closeness.

"There are people, especially family or close friends, who may feel offended that you would need such an agreement and it may strain the relationship. It really depends on the parties involved.

"Do be tactful when asking for money back. Try to do it with a light touch and definitely not bring it up in front of others because it may embarrass the borrower and make things worse," she added.

HOW TO TURN DOWN REQUESTS TO BORROW MONEY

Saying “no” to others can be awkward, especially when the request seems sincere, but Mr Chin reminded lenders that they are not responsible for resolving someone else’s financial difficulties and that lenders should prioritise their own needs.

“You are under no obligation to take on that burden. Setting healthy boundaries is crucial for maintaining your financial stability and fostering balanced relationships,” he added.

Ms Tan said that one way to approach this is to tell the other party it is only right that you would have to discuss it with your spouse, for instance, and if your spouse is not agreeable, it is a valid reason to decline.

If you refuse to lend the money, it will be important to take time to explain your reasons, Ms Lek said. State your care and concern and tell the other party that you appreciate that the person trusts you enough to turn to you for help.

“Explain your genuine reasons for denying the loan. This may range from having your own financial obligations to needing financial security."

You might feel pressured if the other person repeatedly expresses distress, but you can talk about your feelings of guilt while still holding firm to their boundaries, Ms Lek added.

Ms Lee-Cutts said: “Stick to your resolve and keep saying 'no' in a firm but kind way. If the requests continue to a point where you feel harassed, you can politely end the conversation with them.”

Mr Chin recommended that you should avoid arguing to justify your refusal to lend money. Instead, you can empathise with the person and offer a listening ear.

“By doing so, you might be able to maintain a good relationship even when you choose not to provide financial assistance,” he said.

Ms Tan pointed out, though, that no matter what reasons you give, even if they are good and valid reasons, rejection will always hurt the person who is asking. "Rejection can crack a relationship. You have to be prepared to lose friends that way."

HOW TO HELP IN OTHER WAYS

The counsellors said that there are alternative ways to support loved ones without lending money.

"Communicate regret that you can’t help at that point in time, but avoid being too apologetic, and then follow up with non-financial support,” Ms Lee-Cutts said.

Other than listening to their problems, you could help them learn to become more financially savvy.

Ms Lee-Cutts said: “One useful way is to help them write out their budget, set up a spreadsheet, list out debts and identify appropriate financial assistance programmes to approach.”

Ms Lek suggested that you could accompany them to seek help from organisations such as Credit Counselling Singapore or a mental health professional. A social worker could support the family with the stress of the financial strain.

Other practical ways may be offering to take them out for dinner or help them with childcare so that they may cover a few more hours at work, Ms Lee-Cutts said.

However, the counsellors acknowledged that learning to be financially independent takes time and can only be developed with experience.

For Mr Chin, he has established a personal boundary of not providing financial assistance to those dealing with addictions because he understands that giving money will not address the root problem.

“Instead, I explain that financial help is only a temporary fix. Long-term solutions such as seeking counselling support are necessary for improving their life and relationships,” he said.

At Credit Counselling Singapore, Ms Tan said that it holds 90-minute talks every week for people interested to know more about managing debts. Its Info-Talks are held on weekday nights or Saturday afternoons, in person or as a webinar online.

There, participants may ask questions and also learn from what other attendees ask about financial problems and what actions creditors may take, for example.

"It doesn't mean that you have a debt problem if you are attending. You may be there to find out more on how to help a family member or friend, especially if you want to work with and walk with the person who needs help managing finances and debts," she added.

"We have several programmes to address debt repayment, manage money and so on. And if the debt is huge and our programmes are not suitable for you, we help you take stock of your options, for example, maybe explore leasing a room in your home to get rental income."

Helping someone in debt can be a work of charity.

Ms Tan said: "People may tell you they have a medical problem and they are seeing a doctor, but when it comes to money problems, no one will open their mouths.

"So when someone you know is saying to you that he or she is not joining your gatherings anymore because money is tight, or even opening up to you about why they need to borrow money, you may want to direct them to professional help."

The schedule for Info-Talks by Credit Counselling Singapore is available on its website.