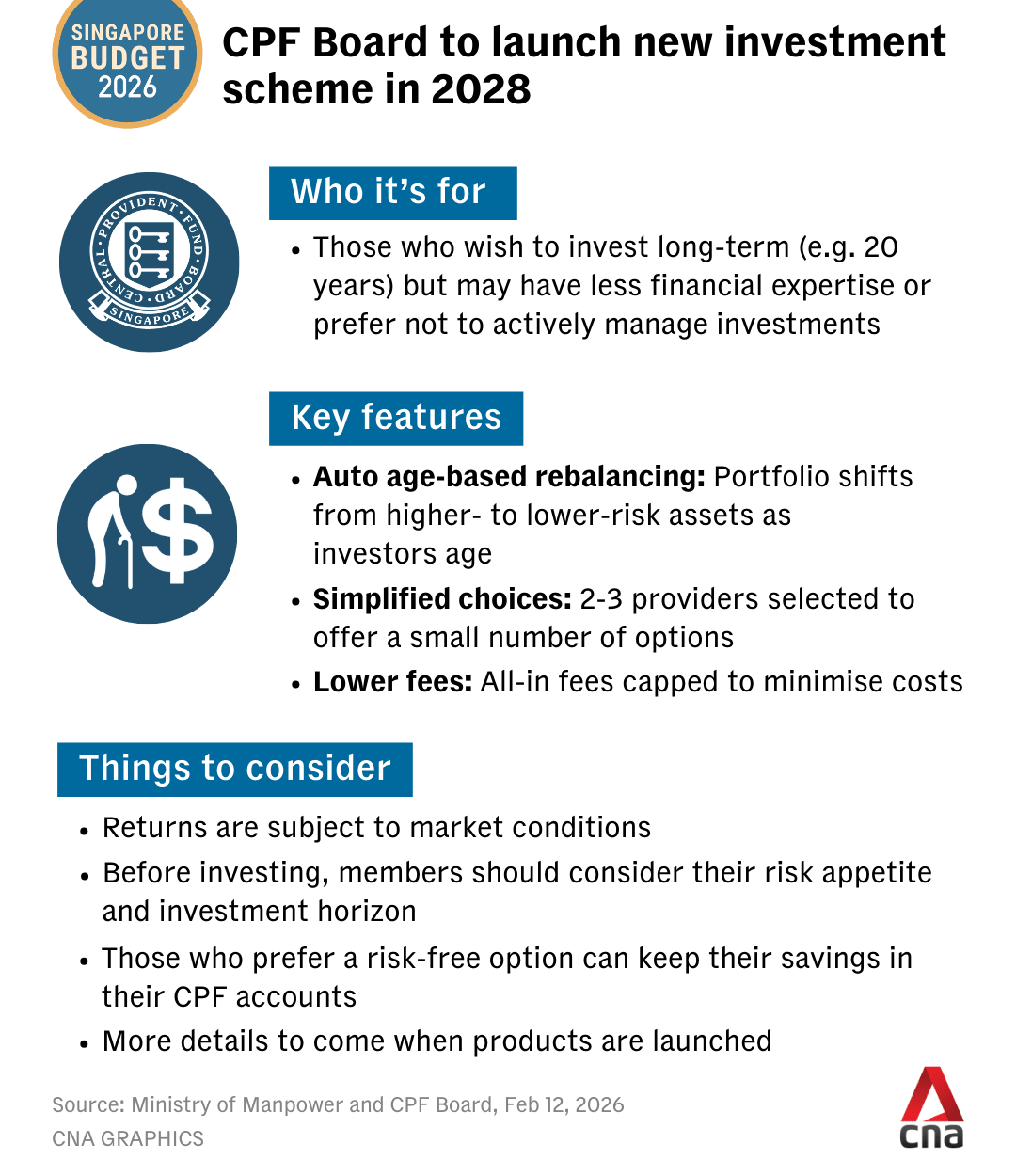

CNA Explains: What the new voluntary CPF life-cycle investment scheme means for you

Who will the scheme be suitable for, and how will it fit in with current options?

The Central Provident Fund Board logo seen on a building in Tampines. (File Photo: CNA/Calvin Oh)

This audio is generated by an AI tool.

SINGAPORE: Central Provident Fund (CPF) members will soon have the option of a simpler, low-cost way to invest their savings when a new life-cycle investment scheme rolls out in 2028.

The voluntary investment scheme was announced by Prime Minister Lawrence Wong during the Budget 2026 statement on Thursday (Feb 12).

It will complement the existing system by catering to long-term investors who are willing to take some risk without having to actively manage their portfolios, the CPF Board said.

CNA looks at how the new scheme will work, and who it might benefit.

How the investment scheme works

Life-cycle investment products work by automatically rebalancing investors' portfolios towards less risky assets as they approach a target date, such as retirement age.

The assets will be progressively liquidated in phases by the target date, for example, when the investor turns 65 and becomes eligible for CPF payouts.

This is to calibrate the investment risk that CPF members are exposed to at different stages of life, and reduce the risk of large losses from exiting during a downturn.

Mr Ling Seng Chuan, head of financial planning, investment and insurance at DBS, said this is known as a glidepath strategy.

"The beauty of the glidepath strategy is it customises to your age. The younger investor gets more exposure to equities and those nearing retirement get the stability from fixed income," he said.

"Having said that, if you start early, you should benefit more from risk and potential return perspective," he added.

Upon liquidation, the investment sale proceeds will be transferred to the CPF member’s Retirement Account up to the full retirement sum. Any remaining proceeds will be transferred to the Ordinary Account.

All-in fees, which include total expense ratio, wrap fees and distribution costs, will be capped to minimise costs and allow investors to retain and benefit from more of their investment returns, the CPF Board said.

Why a new investment scheme now?

The new scheme is a response to the CPF Advisory Panel’s recommendation for the Lifetime Retirement Investment Scheme, which the government accepted in 2016.

The CPF Board said the government had to study ways to offer members a more structured investment option, while striking the right balance between risk and return.

The board noted that several factors now make it timely to introduce the new scheme.

This includes technological developments and the rise of digital platforms, which have reduced the cost of products and have made it easier to automatically rebalance an individual’s portfolio.

Internationally, there has also been a growing adoption of life-cycle investment products, the CPF Board said.

To simplify decision-making for investors, the CPF Board said it is looking to select two to three product providers to offer a small number of options.

“The government’s role is to safeguard investors’ interests through regulatory oversight and act as a gatekeeper for quality investment products, while keeping investment costs low,” the board said.

How would the scheme fit in with current options?

Currently, members can choose to invest part of their CPF savings through the CPF Investment Scheme (CPFIS), which offers more than 700 investment products. There is generally a higher fee cap than the new investment scheme, the CPF Board noted.

The take-up rate for CPFIS has been relatively low. As of September last year, 28.1 per cent of CPFIS-eligible members had active investments in their CPFIS-Ordinary Account. The figure stood at 22.1 per cent for CPFIS-Special Account.

CPF members may also leave their savings in their ordinary account (OA) and special account (SA), which have a base interest rate of 2.5 per cent and 4 per cent per annum, respectively.

Analysts noted that CPF’s new investment scheme offers a middle ground between current options and provides more options for members.

“So if you are the conservative type that does not even want to see any market cycle, you still can keep (your funds) in the CPF OA and SA account … Then if you have a higher, aggressive risk profile, you can participate in the CPFIS,” said Mr Alfred Chia, CEO of financial advisory firm SingCapital.

Most CPF members are likely to be in between, he said, noting that the new scheme can help members improve their long-term retirement adequacy.

He added that while private fund managers will manage the funds, the larger scale of the scheme would allow them to lower expense ratios.

As such, investors would benefit from lower investment costs, he said.

Who will the scheme be most suitable for?

Ms Li Huijing, head of investment management at financial adviser MoneyOwl, said the simplified set of options under the new scheme will be useful for members who wish to take some market risk, but lack the time or expertise to actively construct and manage their own portfolios.

She added that they should also have longer investment time horizons – ideally 15 to 20 years or more before retirement.

“With time on their side, they are better positioned to ride through market cycles and benefit from compounding,” she said.

The CPF Board said there will be no age limit for joining the scheme, although members with a longer runway are more likely to benefit.

Members with a shorter investment runway, including older members, can continue to benefit from risk-free CPF interest rates of up to 6 per cent on CPF balances, it said.

What type of returns can investors expect?

Details on projected returns from the new scheme are not available yet.

In general, potential returns on investments should be commensurate with the risk of the underlying assets, the CPF Board said.

From March, the CPF Board will engage the industry on the product specifications and invite expressions of interest. It will work with independent investment consultants to evaluate applications.

Providers will be required to provide details that include illustrative returns matching the products' risk profiles, the CPF Board said.

DBS’ Mr Ling said such diversified solutions, which are also offered at DBS, are expected to generate about 5 to 6 per cent returns, annualised over the long term. This accounts for strong years and average ones, he added.

Ms Li noted that target date funds in other countries tend to yield around 5 per cent per annum over the long-term, which is broadly comparable to the returns of a balanced portfolio.

“That said, such returns are not guaranteed and the scheme is not risk-free. Returns will fluctuate with market conditions and may not consistently exceed the relatively stable interest rates credited to the Special and Retirement Accounts,” she said.

What should investors consider before applying?

Experts noted that members should consider their own risk appetite before investing.

The investment scheme, as with all investment products, carries risks, and returns are subject to market conditions.

By choosing to invest, members should recognise that they are exchanging government-backed interest rates for market-based returns that may fluctuate, Ms Li said.

“They should be aware of potential drop in market value in the short-term and be aware not to panic and sell at a loss,” she said.

She added that the new investment scheme is designed to be long-term in nature. As such, the CPF savings to be invested should not be needed for shorter-term needs, such as housing.

Ultimately, Mr Chia said that the new scheme not only gives members more options, but also acts as a reminder to start planning for retirement.

“If we have a longer time to actually plan for it and save for it, then retirement planning actually is not difficult. But we have to start early,” he said.