CPF Special Account will be closed for those 55 and above next year. What should you do?

The Central Provident Fund (CPF) Special Account will continue to play a key role when it comes to building up one’s nest egg, personal finance experts said.

The Central Provident Fund's (CPF) Maxwell service centre. (File photo: iStock/TiagoBaiao)

This audio is generated by an AI tool.

SINGAPORE: You may have heard by now that the Central Provident Fund (CPF) Special Account will soon cease to exist for those aged 55 and older.

The policy change to the country’s mandatory social security savings scheme was first announced in Budget 2024. It drew strong reactions online then and was also debated extensively in parliament.

As the implementation date – second half of January 2025 – draws near, it continues to be a topic of discussion at online forums and personal finance conferences on what it means for the retirement adequacy of Singaporeans.

Experts said the impending policy change will disrupt the retirement planning of a small group of older CPF members, but there are ways to adapt.

In the long run, the CPF Special Account will continue to play a key role when it comes to building up one’s nest egg, they added.

A RECAP: WHAT ARE THE CHANGES?

All CPF members below 55 have three accounts – the Ordinary Account, Special Account and MediSave.

An additional Retirement Account is created when an individual turns 55, with money moved there first from the Special Account followed by that in the Ordinary Account.

Currently, the Special Account remains open after the Retirement Account is created. That will no longer be the case from next year.

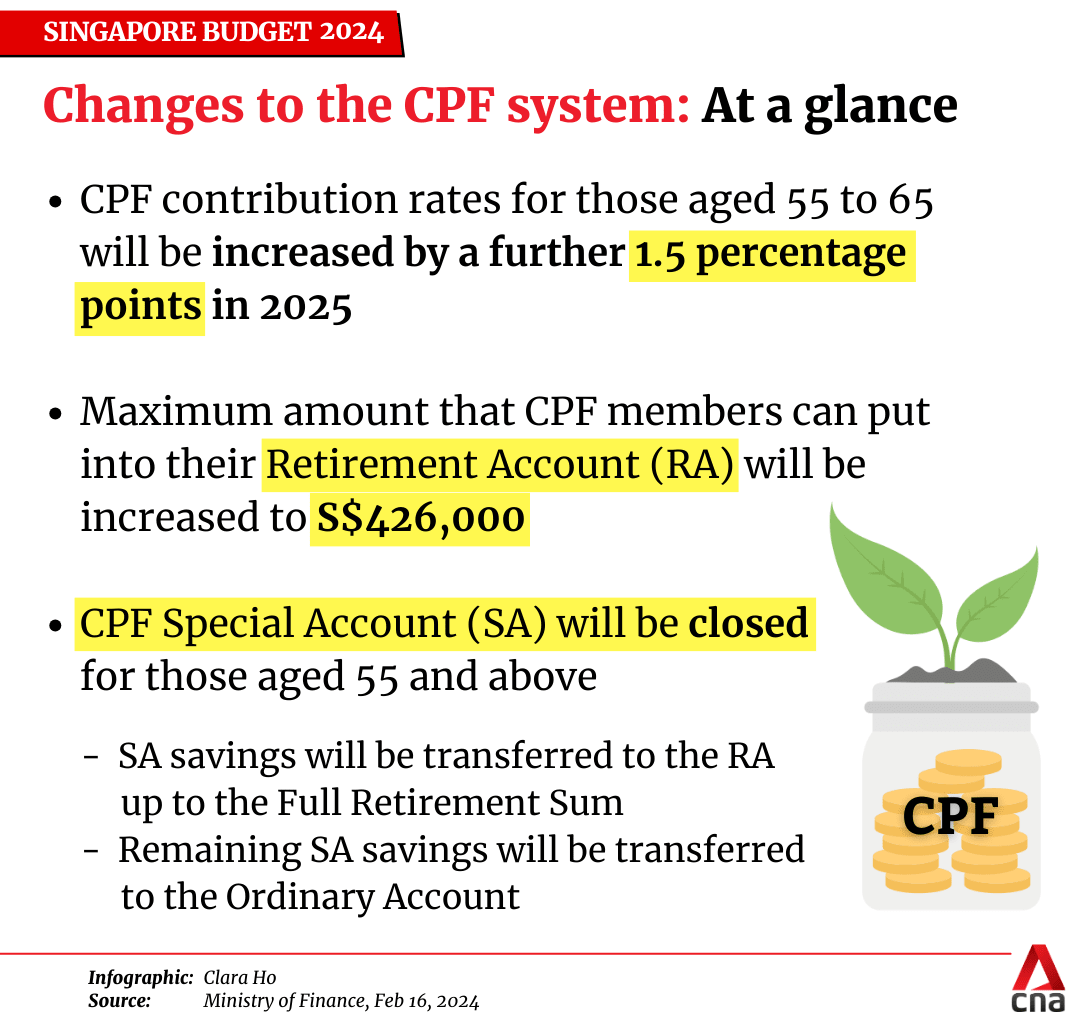

The Special Account will be closed on a person’s 55th birthday and the funds will be transferred to the Retirement Account, up to the prevailing Full Retirement Sum.

Excess funds, if any, will go to the Ordinary Account which offers an interest rate of 2.5 per cent a year. The Special, Retirement and MediSave accounts currently earn per-annum interest of 4.14 per cent.

This is why some have lamented the loss of the Special Account for its higher interest rates. It also allows more on-demand withdrawals from the age of 55 compared with the Retirement Account.

At the same time, the maximum amount people can put in their CPF Retirement Accounts to accrue interest and receive retirement payouts will be raised.

The Enhanced Retirement Sum will be pegged to four times the Basic Retirement Sum from Jan 1, 2025, up from the current three times.

These sums are retirement targets set by the CPF Board, with each unlocking different tiers of monthly payouts 10 years later. They are adjusted annually to account for inflation and other factors.

The smallest is the Basic Retirement Sum, followed by the Full Retirement Sum and Enhanced Retirement Sum.

For 2025, the Basic Retirement Sum is S$106,500 (US$79,200). In turn, the Full Retirement Sum, which is twice the Basic sum, is S$213,000 and the revised Enhanced Retirement Sum will be S$426,000.

IF YOU ARE TURNING 55 SOON …

Not everyone will be affected.

Only those who have accumulated “significantly” more than the Full Retirement Sum in their Special Accounts will feel an impact from the policy change, said Mr Loo Cheng Chuan, the founder of local personal finance movement 1M65.

He recalled how the movement’s Telegram chat group was flooded by questions when the announcement was made.

The 1M65 movement teaches couples how to save S$1 million in their CPF accounts by age 65. Understandably, some of its members will be affected by the upcoming rule change, including Mr Loo who turns 55 in three years.

“When it was first announced, there were many questions. Even I took some time to understand the implications but after that, I realised it’s not too bad a deal,” he told CNA, citing other existing CPF rules that will ease concerns about the loss of flexible withdrawals.

These include provisions that allow members born in 1958 and after to withdraw up to 20 per cent of their Retirement Account savings – excluding cash top-ups, CPF transfers and government grants – after they turn 65.

“These will still allow you to draw out some money – not the full amount but still a significant sum that will be enough for most people,” said Mr Loo.

In the meantime, those who wish to squirrel away more in their CPF to receive higher retirement payouts will now be able to do so.

“Raising the Enhanced Retirement Sum … will be safer for retirement, and it is something that those who are CPF-rich can take advantage of,” said Mr Loo. “The loss of liquidity is exchanged by an increase in payouts – I think that’s okay.”

But top-ups to the Retirement Account cannot be reversed so individuals will need to consider their liquidity needs and financial situation, experts said.

On what other options can be taken by those affected, Mr Christopher Tan, founder-CEO of wealth advisory firm Providend, said it will depend on what the money which would have been left in the Special Account was intended for.

If it was meant to be drawn down for use after 55 years old, the difference between leaving the money in the Special Account versus the Ordinary Account is minimal, he added.

Mr Tan cited an example of a 55-year-old who intends to withdraw S$3,000 each month from his Special Account, which has S$200,000 left after fund transfers to the Retirement Account.

Under current rules, he will be able to leave the balance in the Special Account where monthly withdrawals can be made over 5.7 years. But with the policy change, the sum will go to the Ordinary Account and last the individual for five-and-a-half years instead.

If the drawdown is less frequent, Mr Tan noted that part of the money can be placed in short-term cash-like instruments, such as fixed deposits, if returns are “meaningfully higher” than that offered by the Ordinary Account.

Individuals can also choose to invest the excess funds that are transferred to their Ordinary Accounts.

As with all investments, decisions should be assessed based on one’s risk appetite and investment time horizon.

“For someone who is at the age of 55, the time horizon would be shorter than a younger individual hence the general rule of thumb is to invest in safer options. For example, bonds, rather than stocks,” said Mr Gerald Wong, founder of investment advisory platform Beansprout.

“But also bear in mind that at 55, when compared to the longer life expectancy of Singaporeans, there is still a decent runway so it doesn't mean that people cannot afford to take any risk in their portfolios,” he said, stressing that the key is to be informed of the different investment options and weigh it against one’s risk appetite and investment time horizon.

Mr Loo said there is no need to rush to decide.

“There may be new products by banks and other financial institutions, so sit back and take a few months to see what will be available. If nothing happens, it’s not too late to decide then.”

IF 55 YEARS OLD IS SOME TIME AWAY …

Even if retirement is nowhere near, the impending change is just as relevant given how the CPF can be a “significant part” of one’s retirement savings, said Ms So Sin Ting, chief client officer at digital wealth platform Endowus.

Employees below 55 years old contribute one-fifth of their monthly wages to their CPF accounts. With the CPF monthly salary ceiling going up to S$8,000 by 2026, this means even more CPF savings for some.

Listen:

Add on the advantage of time which amplifies the effect of compounding, young people should make better use of their CPF. In particular, the Special Account for its “risk-free” interest rate of at least 4 per cent, experts said.

“I don’t think there is another option that’s capital and interest guaranteed, so you would want to make use of the Special Account to grow your money,” said Mr Tan.

“Ideally by the time you’re 55, you have accumulated quite a bit in your Special Account and may have to decide if you want (the excess) to remain in your Ordinary Account,” he added.

“But it’s a good problem, right? Because this means you have accumulated a comfortable sum (that gives) you the freedom to decide what to do.”

For those who can, Mr Loo recommend topping up one’s Special Account “as quickly and as much as possible” to reap the benefits of compounding.

Options to boost one’s Special Account savings up to the prevailing Full Retirement Sum include cash top-ups that offer annual tax reliefs of up to S$8,000 and fund transfers from the Ordinary Account.

Again, bear in mind that these moves are irreversible so it will be essential to decide based on one’s liquidity needs, such as plans to tap on Ordinary Account funds to buy a property, said Mr Wong.

Investing is another way for younger people to grow their CPF savings.

Citing figures from CPF's website, Endowus noted that S$27.2 billion in Ordinary Account funds was invested through the CPF Investment Scheme as of June 2024, representing “a fraction” of the S$180.9 billion in Ordinary Account balances.

A “significant portion” of the invested amounts is also in risk-free assets such as Treasury bills.

“This represents a large untapped opportunity to more meaningfully grow our CPF balances towards our retirement,” said Ms So.

She added that those with excess funds in their Ordinary Accounts can consider investing “in a risk-appropriate, low-cost portfolio of globally diversified equity and/or bond unit trusts” with a long-term view.

“Given that CPF contributions are consistent and can only be withdrawn much later in life, young CPF members should be less anxious about short-term market volatility as they can afford to ride through different market cycles for higher expected returns,” Ms So said.

What about those who are no longer in their 20s and 30s and have a comparatively shorter time horizon to ride out market cycles?

Investing is still possible, said Mr Tan who recommended liability matching – an investment strategy that matches investments based on the timing of expected future expenses.

“This means planning early for your cash flow during retirement,” he explained. “For example, think about how much do you think you need for the first five years, followed by the next 10 years and 20 years.”

Money needed for the immediate years of retirement should be put into safer financial instruments. The rest that may not be needed in the short term will then have a longer time horizon and can be invested in riskier assets, like equities, Mr Tan said.