IN FOCUS: Financial Independence, Retire Early - how the FIRE movement goes beyond extreme sacrifice

Some believe FIRE is a mindset of financial prudence, while others see it as a way to give themselves options. Detractors believe the sacrifices required are too extreme. CNA takes a deep dive into the personal finance movement redefining many lives.

FIRE is a personal finance movement defined by frugality, extreme savings and investment. (Illustration: Rafa Estrada)

SINGAPORE: You work in the heart of the central business district, but limit your lunch to S$5 per meal, typically at a food court. You also often carry your own water bottle so you don't spend money on drinks.

Sometimes, you even take the trouble to walk from your office in Raffles Place to Hong Lim Market and Food Centre in Chinatown to save S$1.50. There, you make a beeline for your favourite economic rice that costs S$3.50.

If there are times you spend a bit more on a meal, you balance it out by spending less on your next meal.

And forget expensive CBD coffee. Your caffeine fix comes straight from the coffee capsules provided by your office.

Public transport is your best friend. If you need to take a private-hire vehicle, you compare prices across various apps and make sure to utilise your credits accumulated from using the app to pay for meals and other items.

Such a routine to save money may be familiar to many young working professionals during weeks when they feel more financially stretched. But this is 27-year-old Benedict Tan's regular weekday.

After all, Mr Tan is five years into his FIRE (Financial Independence, Retire Early) journey. He started to pursue FIRE when he landed his first job fresh out of university, as he wanted to get his finances back on track after depleting his savings to pay for his tertiary education and university exchange programme.

FIRE is a personal finance movement defined by frugality, extreme savings and investment.

The aim is that someone who achieves FIRE can use their investments or passive income to cover the expenses associated with their current lifestyle.

Mr Tan's practice of carrying his own water bottle to save money on drinks is not new. The habit was instilled in him and his siblings since young whenever his family went out for meals.

“I was taught that money is hard-earned and should be carefully managed and spent. My dad is an entrepreneur in the timber business and my mom runs her own business in the beauty industry. Raising four children was not a financially easy task and they made many sacrifices so that we could access education resources including tuition,” he told CNA.

“The concept of frugality resonates strongly in me due to my upbringing. And I strongly subscribe to the concept of investing; I believe that only by creating a strong financial base can one truly attain financial independence.”

Under his FIRE plans, Mr Tan’s longer-term goal involves achieving a passive income of S$5,000 a month by the age of 40. He plans to attain this by amassing a S$2.4 million portfolio with 2.5 per cent dividends per annum, calculated based on potential expenses such as mortgage for a Built-To-Order (BTO) flat and daily expenses for food, transport and utilities.

Mr Tan, who is a manager at the Investment Management Association of Singapore, acknowledged that certain people may have it easier due to their "privilege".

But circumstances shouldn’t alter FIRE’s underlying concept: One should strive to increase cash inflow and reduce outflow.

A PANDEMIC-LED RESURGENCE

While it may seem FIRE only recently took the personal finance world by storm, its main ideas originated from the best-selling 1992 book, Your Money or Your Life: Transforming Your Relationship With Money and Achieving Financial Independence.

Fuelled by the influx of blogs, podcasts and online discussion forums in the early 2010s, FIRE then quickly morphed into an aspirational lifestyle, particularly among millennials.

In Singapore, the boom of financial bloggers and personal finance platforms, from Seedly to The Woke Salaryman, around the second half of the 2010s presented finance concepts using vibrant infographics and relatable comics. This further encouraged a spike in interest in personal finance.

And within the last year of the COVID-19 pandemic, the Great Resignation wave prompted people to think more deeply about the sort of life they wished to have, which may have led to a resurgence of FIRE, experts suggested.

“I think the resurgence stems from the fact that people are now going back to hard days of work after working from home. And the draw to FIRE stems from the fact that they’re in the wrong job,” said Mr Loo Cheng Chuan, the 50-year-old founder of local personal finance movement 1M65.

“The FIRE movement picks up when pain at work increases. Now that work-from-home is over, the good days are over. You have to go back to the office, bear with the inconvenience of travelling and the crowd. People start wondering if this is the kind of life they want. They get disillusioned.”

Likewise, CEO of leadership training consultancy Forest Wolf, Ms Crystal Lim-Lange, has observed a “post-traumatic growth” phenomenon contributing to the rise of FIRE.

“Often after a traumatic event, like the pandemic in this instance, people who have seen or experienced suffering have an ‘awakening’ where the challenging event triggers them to reflect on their core beliefs and see new possibilities in their life. For instance, they feel that they now have the courage to walk away from an abusive relationship or quit a job in a toxic working environment,” the 42-year-old said.

“The appeal of FIRE for many is not that they don’t want to work anymore, but that they wish to have meaningful and fulfilling work that they can be proud of.”

Co-founder of personal finance blog The Woke Salaryman, Mr He Ruiming, suggested that FIRE’s reignited popularity could be because the financial markets did “really well” last year.

“During the cryptocurrency phase, I think many people thought they could get into FIRE. So coupled with the Great Resignation, suddenly FIRE became a perceived reachable dream for a lot of people,” he said.

Financial blog Investment Moats founder Kyith Ng has also noticed more people requesting financial planning at the firm where he holds a full-time job.

That said, he noted, the FIRE movement is more extreme than standard financial planning.

FACTORS TO ACHIEVING FIRE

Many people pursuing FIRE today swear by “the 4 per cent rule”. This rule refers to the portion an individual is assumed to withdraw from one’s retirement portfolio within the first year.

Under the 4 per cent rule, one should thus aim to set aside a retirement portfolio amounting to at least 25 times their estimated annual living expenses.

Ms Lim-Lange noted that those who are successful at hitting conventional FIRE goals tend to be “high performers, normally in tech or digital service sectors where they can work remotely and are able to take on more gigs to augment their income”. And they are usually childless, which gives them the “bandwidth” for second or third jobs.

“They also have less financial obligations, communicate well in written or virtual contexts, and (are) ultra disciplined with their consumption or spending in the present,” she added.

As circumstances differ, however, it is important to acknowledge that everyone has a “different starting point”, noted Mr Christopher Chong, who runs the YouTube channel Honey Money SG.

The 31-year-old, who dishes out financial advice on his channel, said generational wealth would result in a headstart for some people and thus enable them to retire earlier. This “wealth” might not just encompass money; it could also refer to a family’s network.

Nonetheless, once the average FIRE enthusiast is armed with clear and tangible goals, they would begin their road to financial independence – only for many to get burnt at the start. These individuals assume they can drastically change their spending habits overnight.

“A lot of people think that they can cut down on expenses immediately. Sometimes, they have a culture shock. Your lifestyle cannot go down so much so fast,” said Mr Ng from Investment Moats.

“It’s not just about the income; it’s your expenses. The biggest factor in all this is what we consider your savings rate – the ratio between how much you save versus the income you get. Usually, for those who aspire to retire early, their savings rate is 40 per cent or higher.”

For example, 42-year-old Mr Ng doesn’t have “strong urges” to travel frequently, making his saving habits “a bit different from other people”. He also already harboured a “certain prudent streak” when he started working.

The struggle to pursue FIRE often stems from keeping one’s expenses the same even when income increases, echoed Mr Chong.

“High income normally does not tally with low expenses, because people believe that when they have a higher level of income, their lifestyle will inflate, then they will need to buy nicer things … to impress other people or to show off their social status,” he said.

“Not many people are willing to break through the barrier which is to keep your expenses the same as you increase your income. Then you will have surplus, and you will start to build wealth, because you start to look at things that you can invest in.”

Many believe that the ideal FIRE candidate is single with a sizeable income, so they wouldn’t have to compromise on their quality of life. But Mr Ng said it doesn’t mean a couple with children cannot pursue or achieve FIRE.

One way is to strive for its less extreme versions, such as Coast FIRE or Barista FIRE.

When regular FIRE doesn't work for you

Coast FIRE entails setting aside enough in investments to take care of your retirement, then leaving it on “autopilot” to gather compound interest so you can “coast”.

Barista FIRE is similar to Coast FIRE. But instead of amassing enough investments to pay for one’s expenses throughout retirement, you build up a portfolio to cover your basics then work part-time to cover the rest.

“I always tell people that the most balanced kind of lifestyle scheme is Coast or Barista FIRE, where you manage to accumulate enough that you can move to a less stressful job which you can also identify with better. When you’re more in your element, you’re more productive, and that job itself also pays for the expenses,” said Mr Ng.

“You accumulate enough that you don’t have to worry about your traditional retirement at 65. Because that retirement portion is a big liability people are trying to save for, and you’ve settled that already. You’re basically happier.”

Another key to pursuing FIRE with a family in tow is to share the same financial principles as your partner, said a couple who have two children.

Mr Chan Jun Hwa and Ms Kamenii Purushothaman, who are both 37, believe that “discussion and compromise” must guide the couple. They run a blog, Sipping Coconuts, about their FIRE journey.

“I think in a couple, in a family, finances are something that should be talked about. If there are great differences in financial goals, then it can be quite difficult for one person to pursue FIRE alone. … In the end, it’s just a matter of how big the nest egg needs to be,” said Mr Chan, who holds a job in finance at a shipping company.

His wife, Ms Purushothaman, who works in business management in the banking sector, takes a “harder stance”.

“I’d say it’s quite difficult for a family to reach financial independence if you don't have shared goals or a shared vision of what the future looks like. (You also need) a similar understanding of each other’s spending patterns. If one person were to have fairly simple needs, and another person has an active social life, (the latter is) definitely (going to be) very expensive,” she said.

“But as long as you have an understanding of what each other is doing, and you are at peace with each other’s spending, then I think you can have a successful relationship and have a successful FIRE. That’s important, because FIRE is going to break apart if your relationship isn’t successful.”

ALL ABOUT OPTIONS

Many of those who spoke to CNA argued for a more nuanced understanding of FIRE. The goal is rarely about stopping work entirely, but rather, about simply having that option.

Investment Moats' Mr Ng noted that many people actually want to “build a sum of money that will give them options in order to give them security”, rather than quit working forever.

“Because what helps them achieve FIRE is that they are very productive people. So their brains cannot rest. Eventually they will need to do some work. It is whether they get paid. That’s where the optionality and security comes in; that is what everyone is looking for, not looking to quit,” he said.

Mr He from The Woke Salaryman shared similar sentiments. He began his FIRE journey around the age of 25 when his mother suffered a stroke while he was holding a job he didn’t enjoy. That period in life “forced” him to look into his finances “very intensely”.

“FIRE was about getting some sort of certainty in life. … So that I can pay for my mum’s treatment if needed, and also one day be able to work in a place of my choosing without having to worry about money. Jobs that I like don’t always pay very well,” the 33-year-old admitted.

“To me, FIRE is just about having the most options available in your life. If you want to work, good. If you don’t want to work, also good.”

And while the married couple Mr Chan and Ms Purushothaman might believe in financial independence, retirement is “optional”.

“For us, what financial independence really means is one word: Options. Options to pursue what we are passionate about and to do that without any financial constraints,” said Ms Purushothaman.

“When we’ve got that aspect covered now, what we’re passionate about could be continuing to work to develop our career aspirations. It could be taking a pay cut to do work that’s interesting or what we’re passionate about, to do volunteer work, or even to stop working to be with our family. Really, the sky’s the limit.”

Listen:

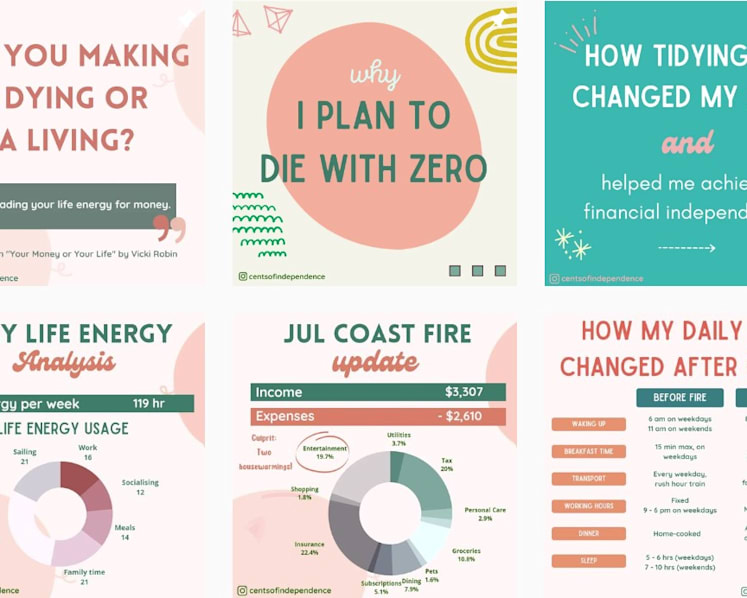

Along the same vein, a former civil servant in her mid-40s who only wanted to be known as Kit quit her job about six months ago, as she wanted to figure out her identity outside of her career.

At the time, she had three years' worth of savings to cover her “basic expenses”, and had already embarked on FIRE in her mid-30s in order to retire by 55. After reading about Coast FIRE, she realised she could execute it now rather than spend a few more years working full-time.

Currently, Kit is “coasting”. She has “enough side jobs to cover current expenses” so she doesn’t need to dip into her portfolio at the moment.

“It’s not that I didn’t enjoy my previous job, but it took up a lot of time. Working is not really 9-to-5. In order to reach your workplace by about 9am, you need to wake up quite early. And by the time you get home after dinner, it’s already 9pm. You’re literally spending most of your time working,” she said.

“After so many years of working, I asked myself, how do I see myself? What do I identify with? What do I enjoy or feel that I’m good at? And I feel like I identified primarily with my job and not much else. I didn’t really spend much time pursuing a lot of other passions or pursuits which were equally important to try.”

Some individuals pursuing FIRE take pride in chasing numbers and growing their portfolio, but Kit was clear from the start that she wanted to “stop chasing (at some point)”.

“If I invest, the outcome should be that I am able to change my life. Like change jobs, stop working, have more free time, do what I enjoy,” she said.

Despite the concern and confusion from ex-colleagues that Kit had to deal with for resigning from a stable job, she remains unfazed as she knows they don’t have the full picture. She has not revealed her FIRE journey to friends and family, except to her partner who fully supports her.

In fact, the main pressure to make her FIRE journey work comes from herself.

“Because I’ve been so prudent my whole life, this is one of the biggest things that I have done. It’s more about trying to justify to myself that I did the correct thing. It’s about living up to my own standards. It’s about trying to live up to these goals that I set up for myself. Because if I don’t go about trying to achieve these goals, then what did I quit my job for?” she said.

“I am my greatest critic. Because I know people don’t know the full story, it’s only me answering to myself. I’d say that’s the most mentally stressful part.”

EMOTION, IDENTITY A BIG PART OF FIRE

To that end, understanding one’s emotions around money is an important part of the FIRE journey. Having a financial plan alone might not be sufficient, one financial adviser told CNA.

Associate director at Finexis Advisory, Ms Ten Huiyu, highlighted that there are financial coaches whose job is to delve into their clients’ relationship with money.

“They talk to their clients about the emotional triggers when it comes to money. Is it from watching your parents? Is it from something traumatic that happened in the earlier part of your life? … They walk their clients through the emotional reaction or connection to money to try to understand their current behaviour,” she said.

Ms Ten believes it would be “very meaningful for each individual to explore their emotional triggers with money”, as she has observed through her work that “quite a lot of (how one manages their finances) comes from their own emotional triggers or experiences when it comes to money”.

“I feel that as I do my work with my clients, yes I can implement or suggest a system to help you achieve your goals, but so many decisions are emotional. It’s not rational. And that derails people from their original goal,” she shared.

“It feels like when the client and I are trying to work on something and an emotional trigger kicks in, it distracts the client, and then we have to start from scratch.”

Those who spoke to CNA also acknowledged that money goes beyond dollars and cents, as someone’s relationship with money can be influenced by other aspects of their identity. They pointed to the notable lack of females openly talking about FIRE in Singapore.

“For men, their identities are very much linked to what they do and how much money they make. So perhaps the pressure is on them … to see how much they can earn, how fast they can earn, and if not then they’re a failure,” said Ms Esther David, 26, who runs her own tuition business.

“I don’t even hear many women speaking about money to begin with, let alone different concepts of money. And that’s something maybe they only discuss in small friend circles.”

Former civil servant Kit, who also runs an Instagram account @centsofindependence documenting her FIRE journey, has observed that males outnumber females in the FIRE space in Singapore. She estimates a ratio of five males to one female based on her experience, adding that females working towards FIRE “might be more low key about it”.

Entrenched traditional gender norms could be another reason behind the gender skew, she suggested. For example, once women have children, many may choose to leave the bulk of financial planning to their husband as caring for their children would be a full-time job in itself.

The host of Honey Money SG, Mr Chong, has noticed a similar trend: About 80 per cent of his YouTube channel’s demographics are male.

Echoing Kit’s sentiment that this could be due to the “social norm” for men to be their family’s breadwinner, he argued for the need to move away from this “very traditional mindset”.

“More women (are realising) they don’t have to depend on men anymore, they can secure their financial independence through their own means. And even if they’re a mother, it doesn’t mean they cannot still go out and work and secure more income for the family,” he said.

Above all, Mr Chong believes FIRE can teach individuals to be self-sufficient.

“I think we have to realise that we cannot always depend on other people. There is always a need to be self-sufficient, be it in money, in careers, in life, anything. I think in order to escape the sandwich generation, people need to learn to take care of themselves first, and that doesn’t matter whether you are male or female,” he said.

“Once you learn to take care of yourself, you will not leave a burden to your next generation, be it your kids or other people who are dependent on you.”

CRITICS WEIGH IN

Yet, neither FIRE’s watered-down versions nor an increasingly nuanced discussion of its benefits have been able to temper often heated criticisms.

A recent CNA commentary about how FIRE is helping millennials redefine conventional ideas of work and finances stated that some people who have become financially independent continue to worry about money, while others find themselves becoming “increasingly stingy”.

“Others resent their golden handcuffs but are afraid a job change will interfere with their financial goals,” said the writer Keith Yap, an economics and development graduate from the Lee Kuan Yew School of Public Policy.

Despite achieving FIRE, these individuals “found no satisfaction in their accumulated wealth”, suggesting that “frugality can diminish the joys of life greatly”, he noted.

Such criticisms are not new to Mr Tan, the 27-year-old who aims to achieve a passive income of S$5,000 a month by the time he is 40. He admitted to receiving occasional flak from friends and loved ones who feel that he is “overly frugal”.

“The most common criticism I get is that life is uncertain, and one should enjoy what money can do, while you still can,” he said.

Even though 26-year-old business owner Ms David aims for financial independence by saving 50 per cent of her salary on good months and about one-third on “not-so-good” months, she doesn’t quite consider herself part of the FIRE movement.

For her, the intangible sacrifices in a bid to pinch pennies don't always add up.

“Many people say if you don’t have something right now, you can have more of it later. That applies very well if you’re talking about material possessions,” she said.

“But what you cannot get back is time. What you are giving up to save the money … is hours with your children, with your friends, with yourself. If you are willing to give up that time, then I think it’s a perfectly sound decision. For most people, it depends on what their priorities are.”

Ms David highlighted that she would probably forgo meeting a certain friend group if she has to spend S$40 at every gathering, but she would not hesitate to hail a cab over taking public transport to a venue if she could save an hour.

“In that one hour, I could answer all my emails and take a bath. It’s not something that profits you, but it does make you feel better enough for the rest of the day,” she explained.

Similarly, Mr Loo, whose 1M65 movement is “superficially the same but fundamentally different” from FIRE, reiterated that FIRE “really involves a lot of huge sacrifices when you’re young”.

1M65 doesn’t require one to “eat bread and water every day”, he said. Instead, it advocates having at least S$1 million in one’s CPF account by 65 by transferring as much money from one’s Ordinary Account to Special Account as early as possible – and the only “sacrifice” required is giving up the dream of owning a condominium or landed property.

Mr Loo is vocal about his support for the “FI” portion of FIRE, but “really disagrees” with the “RE” portion. The latter is “a huge taboo” to him.

“I’m a strong advocate that people should never retire. People say, ‘I want to retire early so that I can travel.’ Come on, how much can you travel? As a financial educator, I teach you how to become rich so that you can now pursue your passion for the rest of your life. Not so you can relax,” he said.

“In my case, I like to be an entrepreneur, but it involves a lot of risk. If I did not have those foundation layers below, I wouldn’t dare to be an entrepreneur; I have kids and loans to pay at that point in time. But because I had those layers, I dare to pursue those passions.”

TRADE-OFFS NECESSARY, BUT IMPORTANT TO ENJOY THE JOURNEY

Although the demands of FIRE are often highlighted by detractors, proponents don’t deny that one must be ready to stomach the sacrifices.

Mr He recalled a comic strip that The Woke Salaryman did, which received backlash for suggesting that different life choices would affect whether someone is able to achieve FIRE.

“The main character (in the comic) was earning a good income, but he chose to live the Singaporean dream. Expensive HDB, two kids, buy a car. These are things that will make FIRE difficult, even though they are not bad things. Which is why I say you should carefully consider the trade-offs,” he explained.

“Some people who think they want to achieve FIRE actually do not want to deviate too far away from the Singaporean dream.”

Pursuing FIRE requires one to make money a “big priority in life”, noted Mr He.

“You will either have to start early, or make some lifestyle changes. You might have to work in jobs just for the money instead of passion or purpose. … Sometimes it involves working to the bone for a couple of years to earn that significant amount of money. If you want a balanced lifestyle, it’s not impossible, but the subset of jobs that will allow you to do that shrinks dramatically,” he said.

“You need a certain level of single-mindedness. You must be able to resist peer pressure. … But, of course, going against the norm is another cost in itself. … I think not many people are ready for such a priority.”

Mr He also believes that all things being equal, a person who places money as a higher priority would “most likely be wealthier” than one who doesn’t.

“And that’s okay. Maybe they are poor in other aspects. Don’t get too hung up on who is better and start comparing. It leads to a lot of unhappiness,” he said.

“Sometimes I do hear people say things like, ‘I’ll never have enough money to retire.’ Then when I ask them how much is enough money, they say it’s around 10 to 15 million. So isn’t a significant part of that a problem you caused yourself?” he added.

“A big part of FIRE is also asking how much you really need to be happy, and whether your happiness is your own version of happiness or what other people want you to have.”

And sacrifices won’t feel like sacrifices if one truly enjoys the journey. This is, in fact, a crucial reason Mr Chan and Ms Purushothaman have made FIRE work for them.

“We’ve always been quite clear that we want to enjoy the journey as well. It’s not just about reaching FIRE and then the journey towards FIRE was unenjoyable because we’re so focused on getting there,” said Ms Purushothaman.

“I don’t feel like we’ve actually made sacrifices; we’ve gone on our holidays, we’ve gone out on our dinners. It’s really about being clear what’s a need and what’s a want for us, and where we are very comfortable spending that money.”

For instance, in their story published three years ago in the Straits Times, the couple revealed that they had saved about 70 per cent of what they believed they needed to retire early. They then sold almost everything they owned in order to travel with their two young sons for a year.

They had done their sums, but still received flak from strangers. Many were in disbelief that the couple’s round-the-world trip was possible with two children, while one online commenter said they “must have stolen money from their companies to fund their lifestyle”, recalled Mr Chan.

The couple understands that such comments are par for the course because outsiders wouldn’t have a full picture of their finances or their family dynamic. What is important is that their everyday decisions remain true to their values.

For example, they don't see themselves upgrading their house or car even though they could afford to because what they have currently works well for their family.

Even when Mr Chan wanted to buy Ms Purushothaman a new phone with a better camera, she objected. For her, being able to make calls and video calls on her phone is “good enough”.

“It’s about not needing something more than what fits my purpose. … Our wants are grounded. Whenever we think about making a big purchase, we always talk about it for quite some time to see whether the desire goes away. I mean, I take a year to buy a blender,” shared Ms Purushothaman with a laugh.

“We don’t really see (sacrifices) as such. It’s more about prioritisation. Some people could see it as a sacrifice not being able to buy a fancy car or the latest iPhone. Maybe for us, having been in this mode for so long, we’ve managed to temper down those wants,” added Mr Chan.

The couple also openly speaks to their children about money. Although they can’t get the world, they “do get a lot of what they want”, said Ms Purushothaman.

“Our answers to why we don’t do certain things for them or put them in certain classes have always been around need versus want … and sometimes, it’s just way too expensive. Like that’s a ridiculous price, I’m not going to pay that even if I was a millionaire.”

Mr Chan also believes that having children does not spell the end of one’s FIRE journey, as he and his wife only started pursuing FIRE seriously after having their firstborn.

He sees FIRE as a set of principles that is worth striving towards, no matter the outcome.

“Not every decision needs to be financially driven. I think children bring a lot of joy to our lives. Does it mean that you may need to work longer? Yes. It just means that you may need to set aside a bigger sum,” he said.

“But FIRE is a mindset. It’s not just a destination; it’s not a race. If it takes you 20 years, fine. Even if you don’t get to retire early, so be it. In the end, just the act of pursuing FIRE will put you in a financially better place than if you did not even embark on this journey.”