Commentary: Inflation rears its ugly head again amid Iran war – how bad could it get?

Singapore’s revised inflation forecasts remain at a reasonably manageable level, but the outlook is still far from clear, says ANZ’s Khoon Goh.

This audio is generated by an AI tool.

SINGAPORE: Singaporeans have been here before. It was just four years ago when the outbreak of the Russia-Ukraine war sent global energy and food prices surging, turbocharging post-pandemic cost pressures and driving Singapore’s inflation to 14-year-highs.

Since then, inflation has steadily eased, offering households some long awaited relief. But that respite now appears under threat. The conflict in the Middle East, stretching into its seventh week, is already feeding into higher energy prices and setting the stage for another near-term acceleration in inflation.

The early signs are visible in daily life. A full tank of petrol now costs at least S$20 more than before the conflict began. The average monthly electricity bill for a four room HDB flat has increased by almost S$2, with a larger adjustment likely at the next quarterly review. Some hawkers intend to raise prices by up to S$1, while taxi and ride hailing operators have hiked fuel surcharges.

Against this backdrop, the Monetary Authority of Singapore (MAS) on Tuesday (Apr 14) raised its inflation forecasts for 2026 to 1.5 to 2.5 per cent, up from 1 to 2 per cent previously.

On paper, this remains a reasonably manageable level of inflation but whether this episode ultimately proves milder than the shock in 2022 – when headline inflation peaked at 7.5 per cent in September that year – is still far from clear as much depends on how the conflict evolves in the weeks and months ahead.

IT’S ALL ABOUT HORMUZ

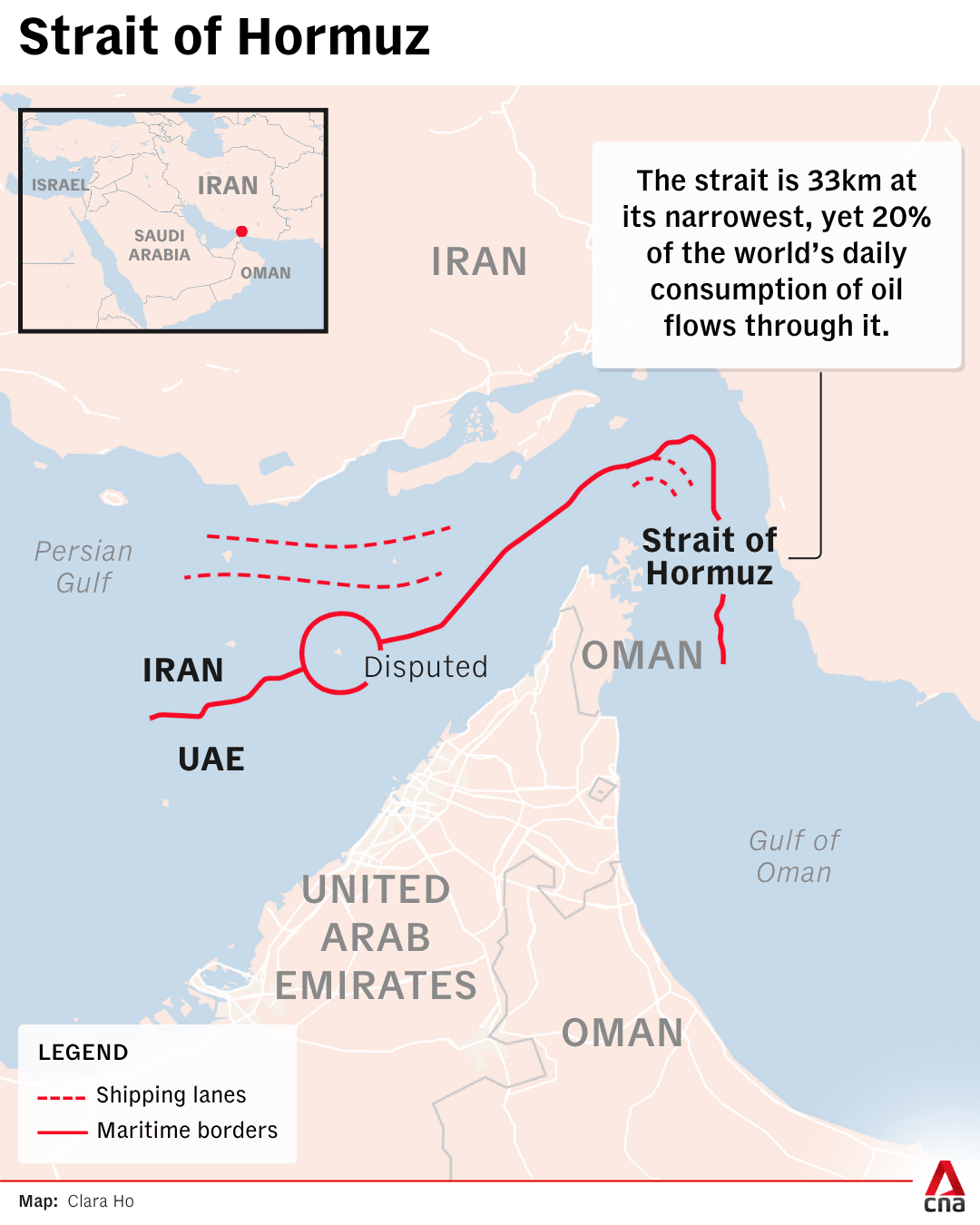

A crucial factor lies in developments around the Strait of Hormuz, through which around 20 per cent of the world’s crude oil supply transits. Hopes of reopening the crucial waterway following a temporary ceasefire quickly faded when weekend talks between the warring sides broke down, prompting a US blockade of all Iranian ports.

While the world has not yet reached a point of outright energy supply shortages, the risk undeniably rises if the conflict drags on.

Already, in the scramble to secure alternative sources, the actual cost of procuring fuel has risen above widely quoted benchmark prices. The result has been a sharp increase not only in petrol prices, but also in diesel and jet fuel. These increases matter because they ripple far beyond the fuel pump.

For instance, diesel, whose prices have surged by about 80 per cent since the conflict began, powers most commercial transport and is a key cost input for shipping and logistics. When it becomes more expensive to move goods from ports to warehouses and to shops, those higher costs eventually show up on consumers’ bills.

The same applies to the delivery of fresh produce to restaurants and hawker centres, as well as food delivery and online shopping. Businesses can absorb these pressures only for so long before passing them on – a process economists refer to as “second round effects”.

Even if shipping through the strait resumes, the global energy market will likely bear lasting scars, such as damage to energy infrastructure in the Gulf.

POTENTIAL ALLEVIATING FACTORS?

There are, however, reasons to believe this inflation episode may not reach the extremes seen in 2022.

Unlike then, we have not seen a broad-based surge in other commodity prices, particularly in agriculture. With Russia and Ukraine also being major suppliers of grains and edible oils, prices of these commodities had surged following the crisis in 2022. Prices of palm oil, for example, more than doubled then.

So far, fertiliser prices have risen by 30 per cent – still around half of the increase seen in 2022 – while higher transport costs will eventually push food prices higher. But the transmission is likely to be slower and more muted than during the post-Ukraine invasion period, when food price inflation was both rapid and highly visible given direct disruptions to global food supply.

It is also worth noting that in 2022, inflation was already on the rise amid a post-pandemic recovery. Headline inflation in Singapore had reached 4 per cent before Russia invaded Ukraine.

In addition, oil prices, while much higher before the Iran war broke out, remain lower than the highs of US$140 per barrel achieved in 2022.

All these could help cap the overall rise in inflation this time around.

WHAT IT MEANS FOR CONSUMERS

Even so, households are likely to be particularly sensitive to any increase in prices.

While inflation measures the rate of change in prices, it is the price level that shapes lived experience. Once prices rise, they tend to remain elevated, with energy prices being a notable exception.

Official inflation figures also reflect a broad basket of goods and services, including items such as electronics and furniture that are purchased infrequently. By contrast, the everyday essentials that dominate household budgets – food, transport and utilities – are rising faster than overall inflation, shaping a sense that costs are climbing more rapidly than headline numbers suggest.

The Singapore government has since responded by committing an additional S$1 billion (US$777 million) to cushion households and businesses from higher energy prices. With public finances in a healthy position, there remains scope for further assistance if conditions worsen.

The MAS tightened monetary policy this week, its first such move since October 2022. Doing so allows the Singapore dollar to appreciate to help dampen imported inflation, and the central bank has scope to tighten further if needed.

Looking ahead, the key message is one of vigilance, rather than panic. For households and businesses, the challenge will be to remain adaptable by managing costs carefully and avoiding overreaction to short term price spikes.

Khoon Goh is the head of Asia research at ANZ.