Asia’s EVolution: Inside China’s grip on battery-grade lithium

This installment of CNA’s series on the forces powering electric vehicles (EVs) in Asia examines China’s dominance in lithium refining and its impact on the global supply chain.

This audio is generated by an AI tool.

SHENZHEN: From city streets across Europe to highways in China and the United States, the global soundscape of traffic is changing - as petrol engines are replaced by electric vehicles (EVs) amid governments’ efforts to cut carbon emissions.

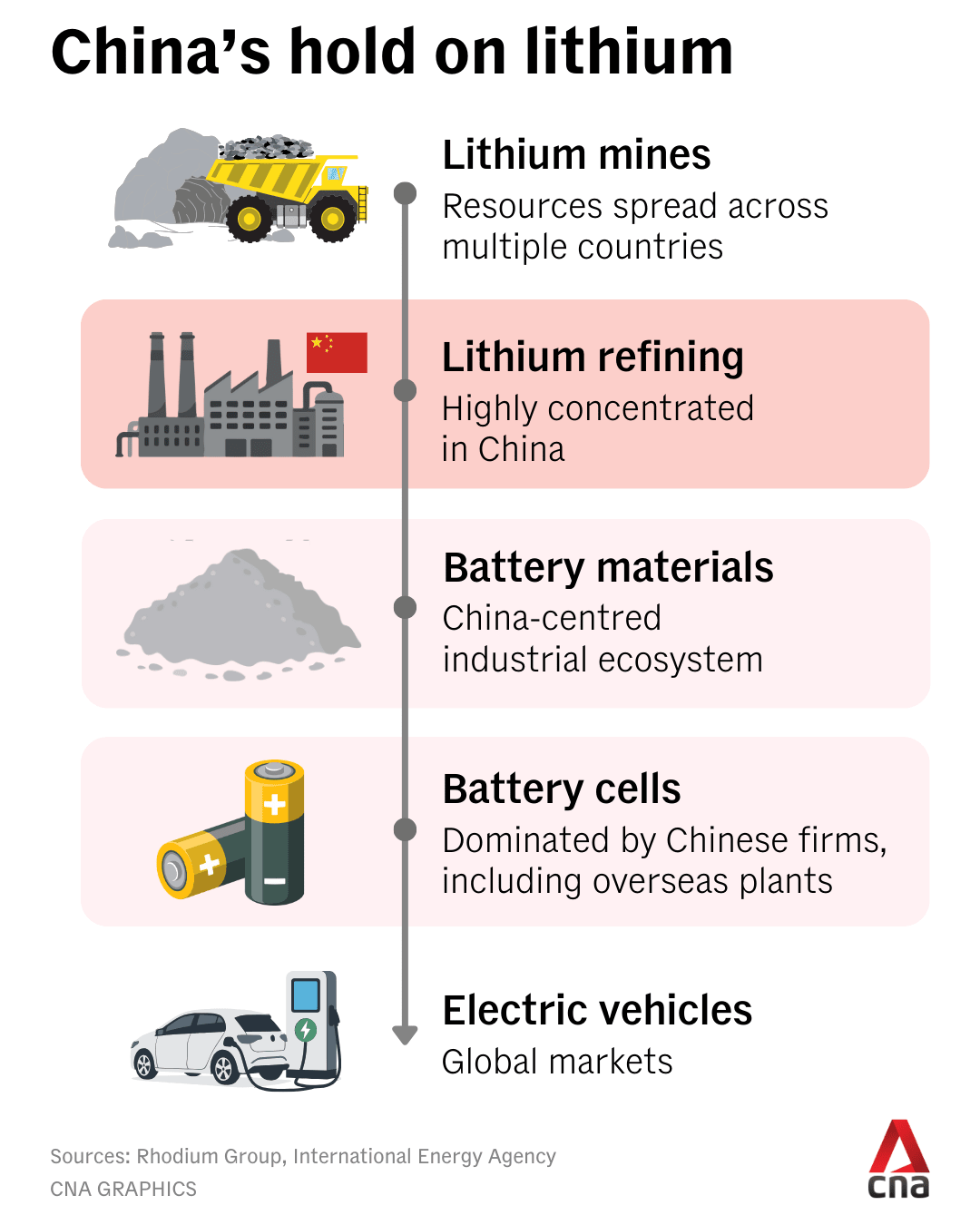

At the heart of this transition are China’s lithium refining hubs. Inside chemical plants, hard rock minerals like raw spodumene ore and brine-based intermediates are stripped and transformed into battery-grade compounds that determine whether an EV battery lasts eight years - or dies out in three.

China is now the world’s largest EV maker, accounting for around 60 per cent of global EV sales in 2025, according to data from London-based price reporting agency Benchmark Mineral Intelligence (BMI) specialising in lithium-ion battery and EV supply chain.

And nearly all electric cars run on lithium-ion batteries.

That has turned lithium into a strategic battleground in the global EV race - but analysts say the real advantage does not lie in owning lithium mines alone.

Instead, it lies in a less visible but critical middle step: converting raw lithium into battery-grade chemicals used by battery and car manufacturers.

China does not have the world’s largest lithium reserves and it isn’t the biggest miner - resources are greater in Australia, South America and Africa.

But BMI estimates that China accounts for roughly 60 to 70 per cent of global lithium chemical refining capacity and output, particularly for hard rock lithium.

“China thus completely dominates hard rock conversion capacity,” said Luc Braun, a research analyst at BMI specialising in lithium and the global hard rock mining ecosystem.

That dominance matters because refining is where costs are set and supply reliability is determined, analysts said.

“At the end of the day, it always comes down to cost,” Braun said, noting that chemical conversion is energy intensive, technically complex and difficult to scale outside China’s established industrial clusters.

THE “WHITE PETROLEUM”

Often referred to as “white petroleum”, lithium is essential to modern rechargeable batteries that power EVs.

The soft silvery metal’s lightweight nature and high electrochemical potential allow for fast charging and efficient energy transfer - making them superior to traditional lead-acid and alkaline batteries.

But it isn’t easy to source.

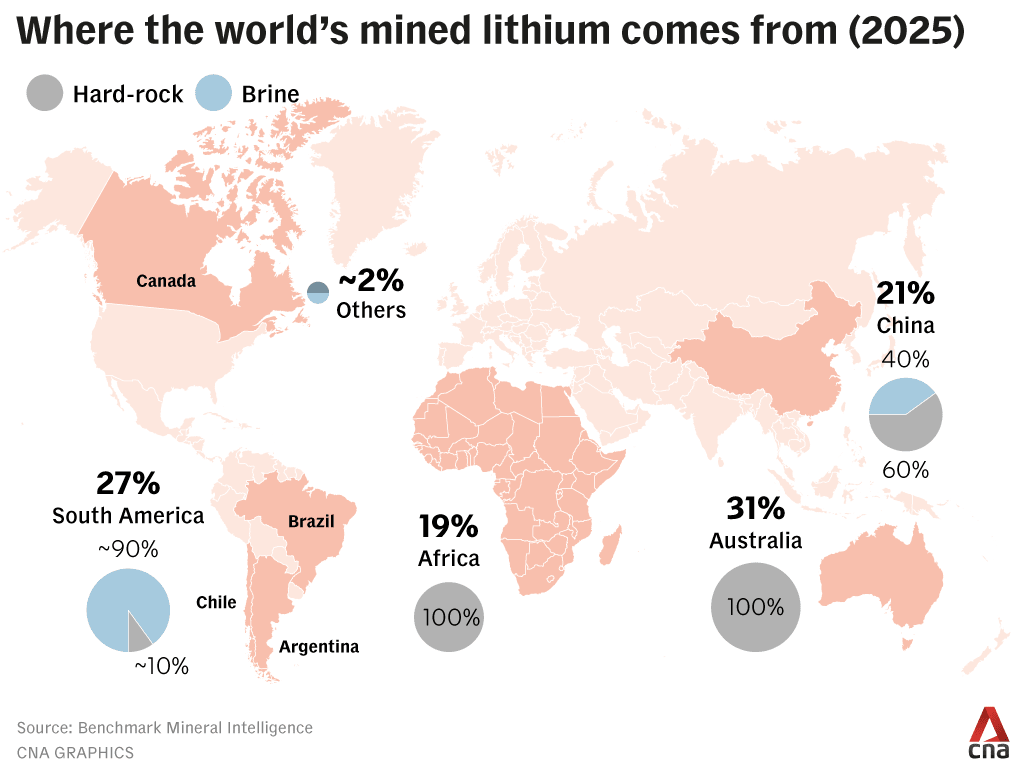

Global supply comes mainly from two sources - hard rock, mined largely in Australia and parts of Africa, and lithium-rich brine extracted from underground salt flats in South America.

In 2025, Australia accounted for about 31 per cent of mined lithium production, followed by South America at 27 per cent, China at 21 per cent and Africa at 19 per cent, according to BMI.

“A mine gives you lithium-bearing rock or brine, but the battery supply chain runs on tight-spec lithium carbonate and lithium hydroxide,” said Srinivas Popuri, a battery value chain and industrialisation expert who advises automakers, gigafactories and investors.

That conversion step is where China’s role becomes decisive.

Once lithium concentrates or brine-based chemicals are produced overseas, much of the material is shipped to China for further processing.

BMI’s Braun said that “the vast majority of chemical output (outside China) comes from South American brine operations, which are typically integrated facilities” - meaning their output is tied to their own feedstock and not available for processing third-party material.

Even then, the work is often unfinished.

Roughly half of this South American chemical output is not to “battery-grade” standard and needs further refining, Braun said, with material often sent on to China for additional processing.

Hard-rock lithium follows a similar pattern - but at a larger scale.

China is a significant lithium miner itself, Braun said, but it “relies primarily” on Australia and Africa for hard-rock feedstock.

Concentrated ore from those regions is shipped to China, where it is converted into lithium carbonate or lithium hydroxide inside Chinese chemical plants.

While refining capacity outside China has expanded in recent years, Chinese firms still dominate both output and capacity, with many newer projects elsewhere operating well below their designed levels, Braun said.

Once upgraded to battery-grade chemicals, lithium feeds into a downstream chain that is also heavily concentrated in China.

China controls around 86 per cent of global cathode active material production and around 85 per cent of battery cell manufacturing, according to BMI data - allowing batteries to move quickly from chemical plants into vehicles - often within the same industrial clusters.

Industry executives said this integration is critical.

A leading Chinese lithium producer who declined to be named told CNA that refining is embedded within a broader manufacturing ecosystem - where equipment suppliers, engineers, chemical firms and battery makers operate side by side, helping drive down costs and speed up production.

Popuri compared lithium refining to oil production.

“Mining gives you crude (oil). Refining gives you petrol and diesel that meet strict specifications and behave predictably in engines,” he said.

“Lithium is similar,” he added.

“You take a relatively messy raw input and convert it into a purified chemical … with tightly controlled impurities and consistent physical properties.”

Even small variations affect battery performance, yield and lifespan, he said - directly shaping costs and supply reliability for carmakers.

HOLDING THE CHOKEPOINT

The refining chokepoint becomes most visible when markets tighten, analysts said, revealing why much of the world still depends on China to turn raw lithium into battery-grade material.

Mine ownership remains critical.

For EV supply security, owning lithium mines matters more than locking in battery-grade chemicals, said YJ Lee, director and fund manager at Singapore-based Arcane Capital Advisors.

He pointed to the supply squeeze during the 2019 to 2022 EV boom, when lithium prices surged and supply tightened.

“When there is a clear and growing deficit and prices are sky-high, even ‘locked-in’ contracts for battery-grade chemicals may fail to deliver,” Lee told CNA.

“Perhaps the mine found a better price at another converter. Or the converter would rather take the penalty on the contract and sell the product at a much higher spot market price - that can and has happened before,” he said.

Those risks have pushed automakers and battery firms further upstream, triggering a wave of mine offtakes and equity stakes.

But that does not change where the system’s bottleneck sits.

“Conversion of hard-rock to chemicals outside of China is minimal,” said Braun.

“This is where the most serious power and capacity imbalance is.”

That imbalance persists, regardless of how it is measured, he added.

“In my opinion, it makes little difference whether you refer to output or capacity - firms in China dominate both,” he said.

While refining projects have come online in the US and Europe, most remain stuck in early ramp-up, Braun notes.

“Those projects that have only recently been commissioned are in their ramp-up phases and have output well below their ‘nameplate’ capacity,” he said.

In recent years, the US and Europe have stepped up efforts to localise lithium refining - backed by subsidies and industrial policy.

Earlier in January, Tesla announced that it had begun operations at its lithium refinery near Corpus Christi, a city in south Texas - designed to produce battery-grade lithium for its own EV production.

Dutch lithium supplier AMG said in late January that it still ships spodumene from Brazil to China for conversion before sending it on to Germany for processing into battery-grade lithium, underscoring how limited non-Chinese refining options remain.

Analysts said such projects signal intent to reduce reliance on China, but are unlikely to materially shift global refining dynamics in the near term.

“To meaningfully reduce reliance on China’s refining ecosystem, the US and Europe need more than nameplate capacity,” said Popuri.

“They need plants that run steadily at high yield - producing consistent battery-grade material that is qualified by major cathode and cell makers and (also) backed by long-term offtake to support financing,” he added.

Even then, any shift will be gradual, he cautioned.

“A realistic timeline for material impact is late-2020s into the 2030s,” he said.

Lee said the challenge is structural.

“What we are seeing is the US and EU trying to build a parallel supply chain to avoid reliance on China,” he said.

“First of all, this will end up being a structurally higher-cost supply chain … Secondly, it will take far longer than the US and EU countries think,” he added.

China’s grip on lithium refining also comes with growing downsides, analysts said, as sharp price swings, overcapacity risks and rising regulatory costs complicate investment decisions across the supply chain.

“When lithium prices crash, projects get delayed and high-cost capacity becomes difficult to finance without strong offtake support,” said Popuri.

Lee described the recent downturn as short but painful.

“It was a pretty painful lithium winter between 2023 to 2025 - but in the grand scheme of things, it was a short one,” Lee said.

Lithium prices fell nearly 86 per cent from their November 2022 peak to a 2024 low - forcing companies around the world to halt operations at mines.

“What did happen was a lack of capital that caused many lithium developers to put a hold on their projects, delaying them by several years,” he added.

Lithium conversion is an energy-intensive chemical process that produces waste and residues, making environmental compliance, permitting and waste treatment an increasingly important part of costs and timelines.

“Only when upstream mine supply is stable can the industry chain develop normally,” the Chinese lithium producer said - adding that costs and process maturity across different stages affect both prices and supply quality.

David Zhang, General Secretary of the International Intelligent Vehicle Engineering Association in Hong Kong, told CNA that the global expansion of lithium refining and battery production capacity - particularly as capacities expand beyond China - is driving a rebalancing of the industry, with volatility and capacity adjustments an expected part of that process.

“There will definitely be overcapacity and price volatility,” Zhang said.

WHAT LIES AHEAD

Analysts said lithium is unlikely to be displaced any time soon, as most alternative battery designs still rely on it as their core ingredient.

“I would say that lithium is very likely to remain central to EV batteries for the next five to ten years because even mainstream alternatives are still largely within the lithium-ion family,” said Popuri.

Rather than disappearing, constraints are more likely to shift within the lithium ecosystem itself, he added.

“What can change is where the bottleneck sits,” he said. “The constraint may move between carbonate versus hydroxide pathways, or towards other midstream inputs and manufacturing yield, rather than lithium ‘going away’.”

Lee said lithium demand is also broadening beyond EVs. “Lithium is now making its way into every product imaginable,” he said.

But higher prices could eventually accelerate alternatives, he added.

“The next scalable technology is definitely sodium, given their similarities with lithium battery production processes,” Lee said.

Analysts said sodium-ion technology is also likely to play to China’s strengths, as it can be produced on adapted lithium-ion production lines within the country’s existing battery ecosystem.

China’s current advantage is likely to hold in the near term, but not indefinitely, said Zhang.

“Based on China’s current advantages, maintaining this lead for (the next) five to ten years should not be a problem,” he added.

“But the bottleneck will change.”