Commentary: Higher CPF monthly salary ceiling is good news for your retirement plan - provided you make the most of it

Amid the debate over the higher CPF monthly salary ceiling, Endowus’ chief investment officer looks at what the changes mean for your retirement income in dollars and cents.

File photo. The long-term impact of a raised CPF salary ceiling has far-reaching benefits that are important to remember. (Photo: iStock/joyt)

SINGAPORE: Since the announcement of a staggered increase in the Central Provident Fund (CPF) monthly salary ceiling, I’ve had many conversations about what it means for Singapore residents and businesses. Those who fall within the S$6,000 to S$8,000 income bracket are worried about the impact on their take-home pay, while business owners are, of course, fretting over the increase in manpower costs.

In the short term, it’s understandable that seeing a drop in one’s monthly take-home pay (assuming the wages stay the same) can feel unsettling - even if that money is going to one’s own CPF. This is especially so if the individual is the sole income earner in the household.

But there is also a timely invitation here for everyone to conduct a broader review of their personal and family finances and budgeting.

The long-term impact of a raised CPF salary ceiling has far-reaching benefits that are important to remember. Commenting on the policy change last Friday (Feb 17), Deputy Prime Minister Lawrence Wong said that “if we don’t start building up for our retirement, we are storing up more problems for ourselves and for society”.

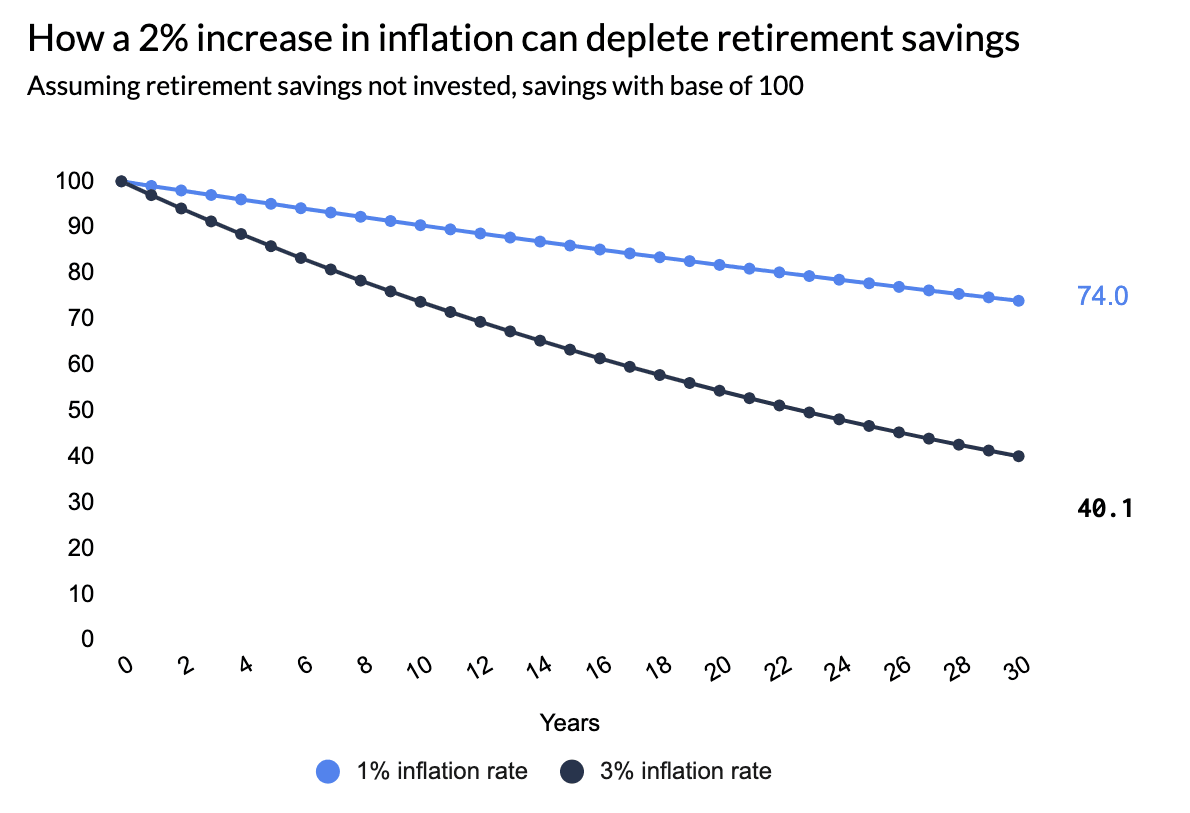

The Government’s concern around retirement adequacy is well-founded, given rapidly rising cost of living pressures. A sustained increase in the long-term trend of inflation from 1 per cent to 3 per cent will lead to an approximately 45.8 per cent decrease in retirement savings over 30 years. A 1 per cent annual inflation rate will reduce purchasing power by 26 per cent over 30 years, while a 3 per cent inflation rate will reduce it by almost 60 per cent.

The country’s headline inflation exceeded 6 per cent and core inflation ended at 4.1 per cent for 2022 - the first time it has exceeded 3 per cent since 2012. We all feel the painful effects of higher prices from last year.

Against this backdrop, more Singaporeans are also worried they may not have enough funds when they retire. The Endowus Retirement Report 2022 found that Singaporeans in middle- to high-income households had the greatest loss of confidence in their retirement adequacy than before. About 42 per cent of respondents in this income bracket said they were not confident in 2022, a jump from 24 per cent in 2021.

Meanwhile, nearly half of all respondents in the same study said they planned to rely on CPF payouts for retirement - an indication that many continue to see CPF as a key source of funds to see them through their golden years.

There have been concerns that CPF Life payouts are not enough for the average Singaporean. With the latest announcement on the higher CPF monthly salary ceiling, the big question is: How much of an impact will this have on an individual’s CPF funds? And will it be enough for one to retire comfortably?

HOW YOUR CPF CONTRIBUTION LEVELS WILL CHANGE

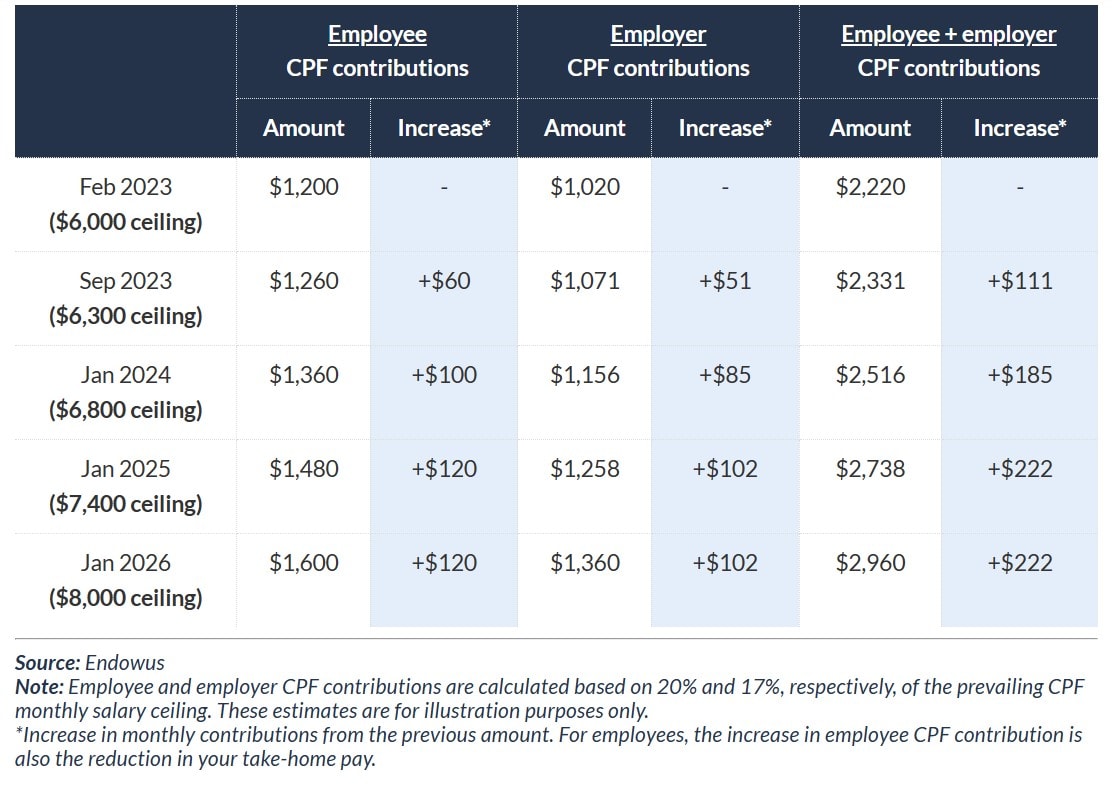

Let’s say you’re an employee aged 55 or below and earning the same salary of S$8,000 per month from now till January 2026. The table below shows how your CPF monthly contributions will change.

By 2026, you will be making an additional S$400 in employee contributions, while your employer contributes S$340 more. In total, S$740 more will be going into your CPF account every month by 2026, as compared to today.

These sums are hardly insignificant, and when compounded at the 2.5 per cent per annum interest rate in the Ordinary Account, they can make a big difference in growing your savings. The larger contributions can be helpful when it comes to financing your housing down payment and mortgage.

Moreover, when stretched over a longer term - of, say, 30 years - the growth of your savings will be substantial.

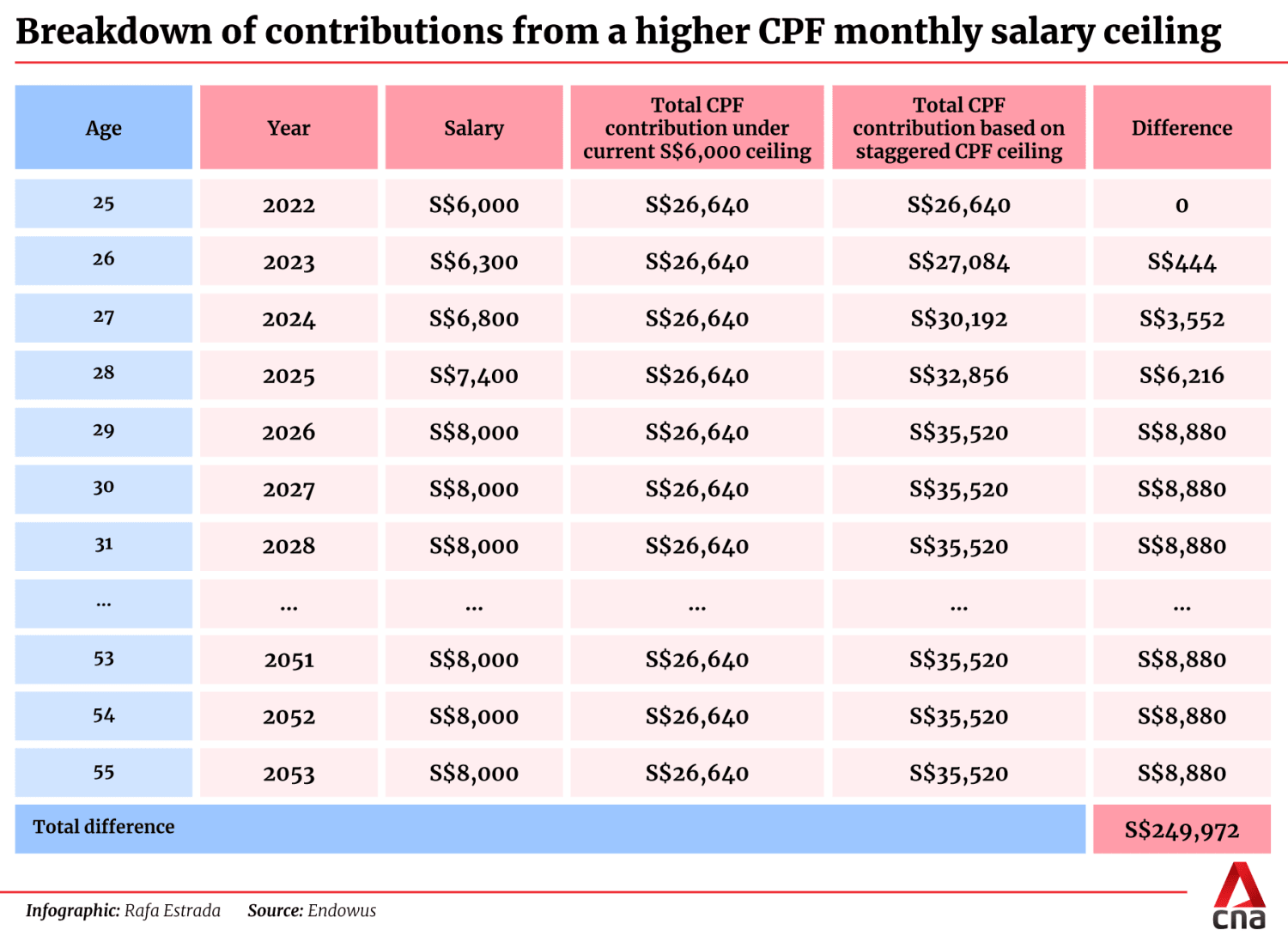

Let’s say a 25-year-old in 2022 earned a monthly salary of S$6,000. This salary then goes up on a staggered basis over four phases, starting from September 2023, to S$8,000 by January 2026 - exactly mirroring how the increases in the CPF monthly salary ceiling will be staggered through to 2026.

By the time this person turns 55, nearly S$250,000 more in contributions would have gone into his or her CPF than if the ceiling had stayed at S$6,000. This figure excludes interest and assumes the S$8,000 ceiling is unchanged from 2026 to 2053.

MORE CAN BE DONE FOR GREATER PEACE OF MIND

The illustration above shows a healthy increase in savings that Singaporeans can additionally tap into for their retirement and housing needs. However, prudent and sustainable financial planning still lies at the heart of ensuring this money will be enough for your retirement nest egg.

Of late, reports have surfaced indicating that Singaporeans are spending more, either on discretionary expenses or relative to their income growth. In October 2022, the Monetary Authority of Singapore (MAS) said that spending on non-essentials will likely be the biggest cause of inflation for 2023.

To top it all off, inflation is expected to stay elevated this year, with analysts predicting headline inflation to average 5.5 per cent to 6.5 per cent. In January, headline inflation edged up to 6.6 per cent, official data released on Thursday (Feb 23) showed.

Note that this is higher than the CPF Ordinary Account interest rate of 2.5 per cent per annum. Taken together, high inflation and unchecked spending can quickly erode the ability to benefit from any increases in salary or CPF account balances.

The only sure way to beat inflation is to invest for the long term. Those who do not plan their finances strategically with a long-term view will eventually have to take off their rose-tinted glasses, and realise that a comfortable, well-funded retirement lifestyle has become out of reach.

Those who have a long runway of more than 15 years to retire can take on some risk and invest some or all of their CPF Ordinary Account savings to make their money work harder and outperform the interest rate.

Depending on their risk appetite, they may want to consider the stock market. For example, the S&P 500 index, which represents the top 500 companies in the US, has performed well historically, with an annualised return of 9.49 per cent between January 2003 and February 2022.

Others may want to choose a disciplined regular savings plan to reduce the volatility of markets and outcomes.

Either way, the best long-term solution to inflation is not just to save fastidiously or get low yields, but to take a long-term view on retirement planning and investing and sticking to a plan that allows you to compound your CPF savings into a meaningful nest egg to secure the long term financial future for you and your loved ones.

This will give you peace of mind and enable you to still afford the higher cost of living in your golden years.

Samuel Rhee is Chairman and Chief Investment Officer at Endowus.