Commentary: Inflation is a silent killer of retirement planning. Here’s what you can do

Amid an ageing population in Singapore, how can individuals make sure they do not outlive their savings? GYC Financial Advisory’s Aw Choon Hui weighs in.

A group of elderly men playing a game of checkers. (Photo: Calvin Oh/CNA)

SINGAPORE: In this world, nothing can be said to be certain, except death and taxes. This quote appeared in a letter American founding father Benjamin Franklin wrote to French physicist Jean-Baptiste Le Roy when discussing the new Constitution of the United States.

We believe that Franklin might have missed a possible third constant element of modern life: Inflation.

It was not too long ago that Singaporeans had a rather apathetic attitude towards inflation but now, inflation has risen as a major topic of worry. What type of price increases can one expect over the long term? How does inflation mess with retirement? And how does one invest to keep up with rising prices?

According to a report commissioned by Prudential and conducted by Milieu Insight in June, one in five Singaporean residents expects to delay retirement by six years, with many concerned about the increasing cost of living.

Amid an ageing population in Singapore, how can individuals make sure they do not outlive their savings?

HOW MUCH IS NEEDED FOR A BASIC STANDARD OF LIVING?

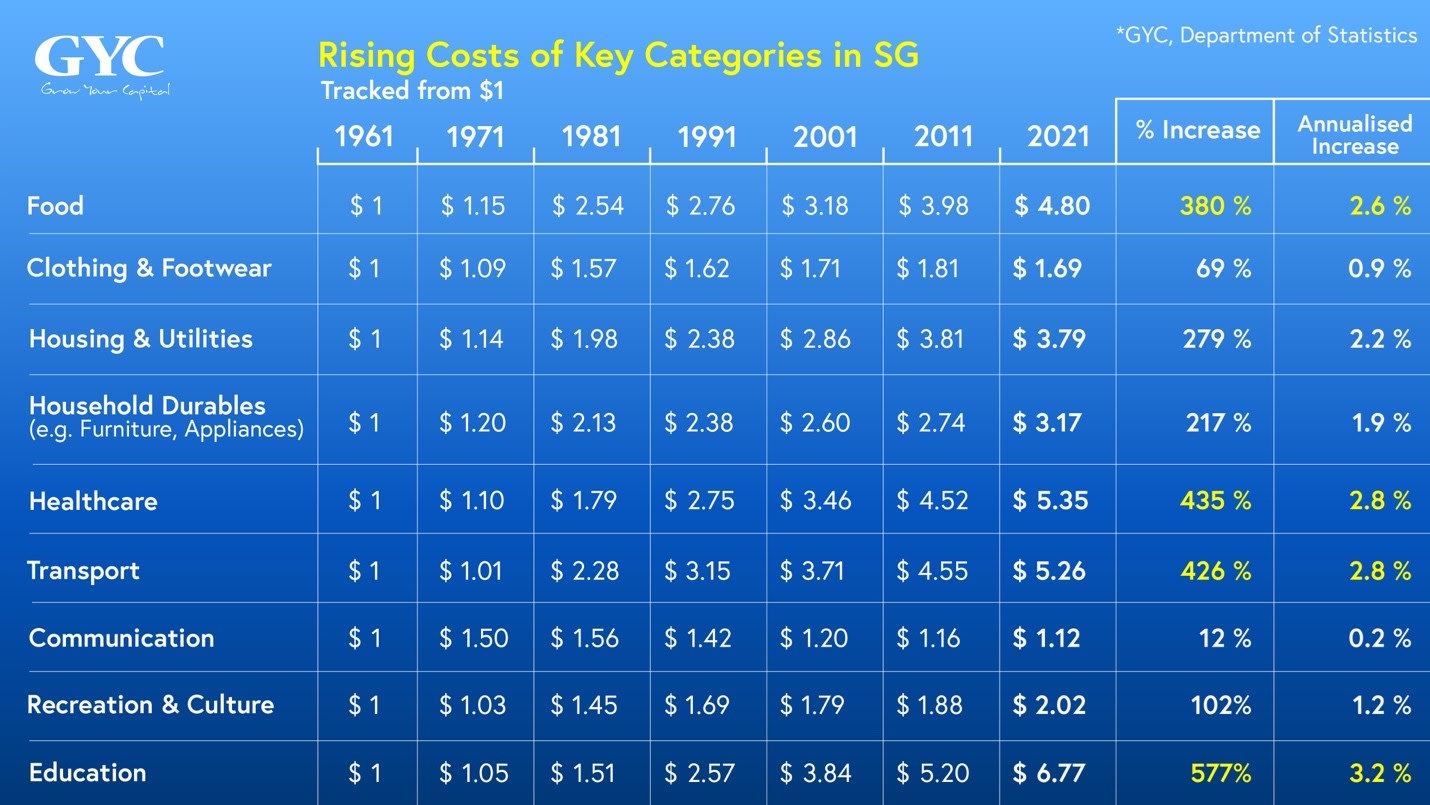

The chart below shows how a dollar’s worth of products has changed over the past 40 years. Among the categories, you will notice that education, transport, healthcare, and food have had the highest price increases over the years.

Another insight is that even with banks dangling higher interest rates in the battle for deposits recently, some come with strings attached and the rates for savers on plain-vanilla accounts are nowhere close to beating inflation.

You could argue that retirees are unlikely to bother with rising education costs, given that their children (if any) are unlikely to be of school-going age. So, what do retirees spend on and what does their typical budget look like? This will depend on how basic necessities are defined and the type of lifestyle they wish to achieve in their golden years.

A study conducted by the Lee Kuan Yew School of Public Policy shed some light on this topic. They identified the amount of income and the list of things needed for a minimum standard of living (by society’s standards). From this, you can then come up with the base income required to achieve that quality of life.

The 2021 study showed that for people aged 65 and older, a couple would need S$2,419 a month, while a single person would need at least S$1,421. The top three expenses would comprise food (29.2 per cent), recreation and culture (19.7 per cent), and housing and utilities (18.4 per cent).

The long-term inflation rates of those categories are 2.6 per cent per annum, 1.2 per cent per annum, and 2.2 per cent per annum. So as a general guide, one should factor in these price increases when planning their future budget.

KEEPING UP WITH INFLATION: A LOOK AT VARIOUS ASSETS

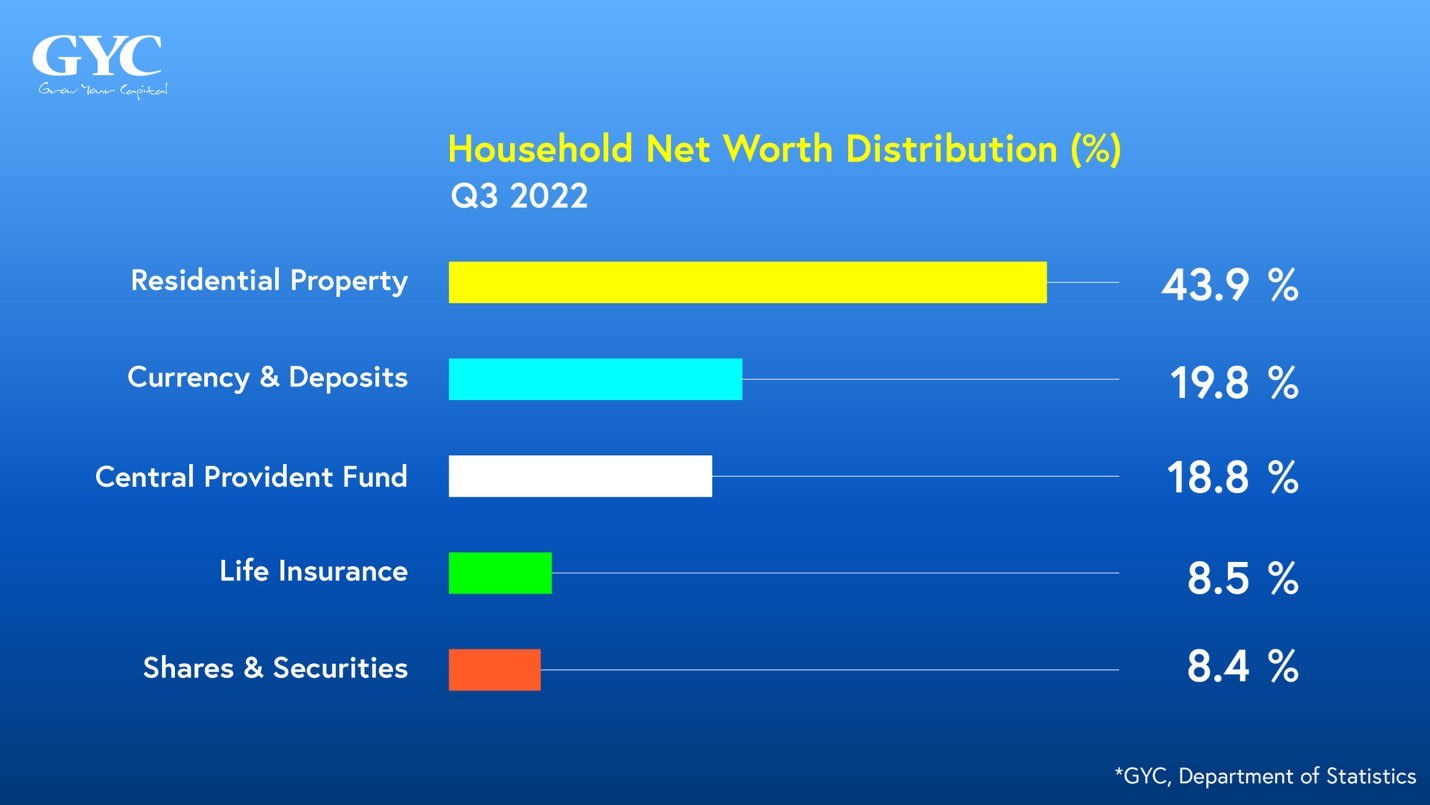

The latest Singapore household sector balance sheet shows how an average household’s wealth is spread. Unsurprisingly, property formed the largest chunk (43.9 per cent) by virtue of property being one of the largest purchases by Singaporeans. The next two biggest holdings are deposits and CPF (19.8 per cent and 18.8 per cent. Shares and securities form the smallest allocation at 8.4 per cent.

This is a problem and here’s why.

In his book, Stocks For The Long Run: The Definitive Guide To Financial Market Returns & Long-Term Investment Strategies, author and finance professor Dr Jeremy Siegel compares extreme long-term total real returns (i.e. returns from investment plus any income or dividends received, minus inflation) of various asset classes.

He makes the case that among all asset classes, a broadly diversified stock portfolio provides the best chance for investors to preserve their wealth against inflationary shocks, nearly doubling in purchasing power every decade.

However, most people tend to fear the short-term swings in stock prices which are driven by a multitude of factors like fear and greed, and thus prefer safer investments and cash deposits.

As a result, they miss the broad upward trend in stock returns, thus underperforming inflation which insidiously erodes their wealth over the years.

WHICH ARE THE BEST ASSETS TO BEAT INFLATION?

Research also shows which areas of the market have the best chances of maintaining one’s purchasing power over the years. In a 2021 paper, Dr Wei Dai and Dr Mamdouh Medhat from investment giant Dimensional Fund Advisors studied the relationship between inflation and the performance of global asset classes such as stocks, bonds, commodities and REITs.

The data measured real returns (actual return minus inflation) and showed that while returns from most asset classes were able to outpace inflation (which averaged 5.49 per cent in the US during high inflation years), there were clear winners.

The only asset class which had a negative outcome were short-term treasury bills – equivalent to fixed deposits. This reinforces Siegel’s data earlier, showing that stocks provide the best chance of keeping ahead of inflation whereas holding currency in the form of deposits or CPF will lead to a gradual erosion of one’s purchasing power.

Listen:

WHAT ABOUT PROPERTY?

Singaporeans are generally property crazy and see owning real estate as the sure-fire path to long-term wealth. Many property investors further claim that it is a good hedge against inflation.

On the surface, this appears to be a reasonable assumption. With a growing population, a finite supply of land, and the rising input prices of raw building materials, the value and rental yields on property should theoretically rise with inflation.

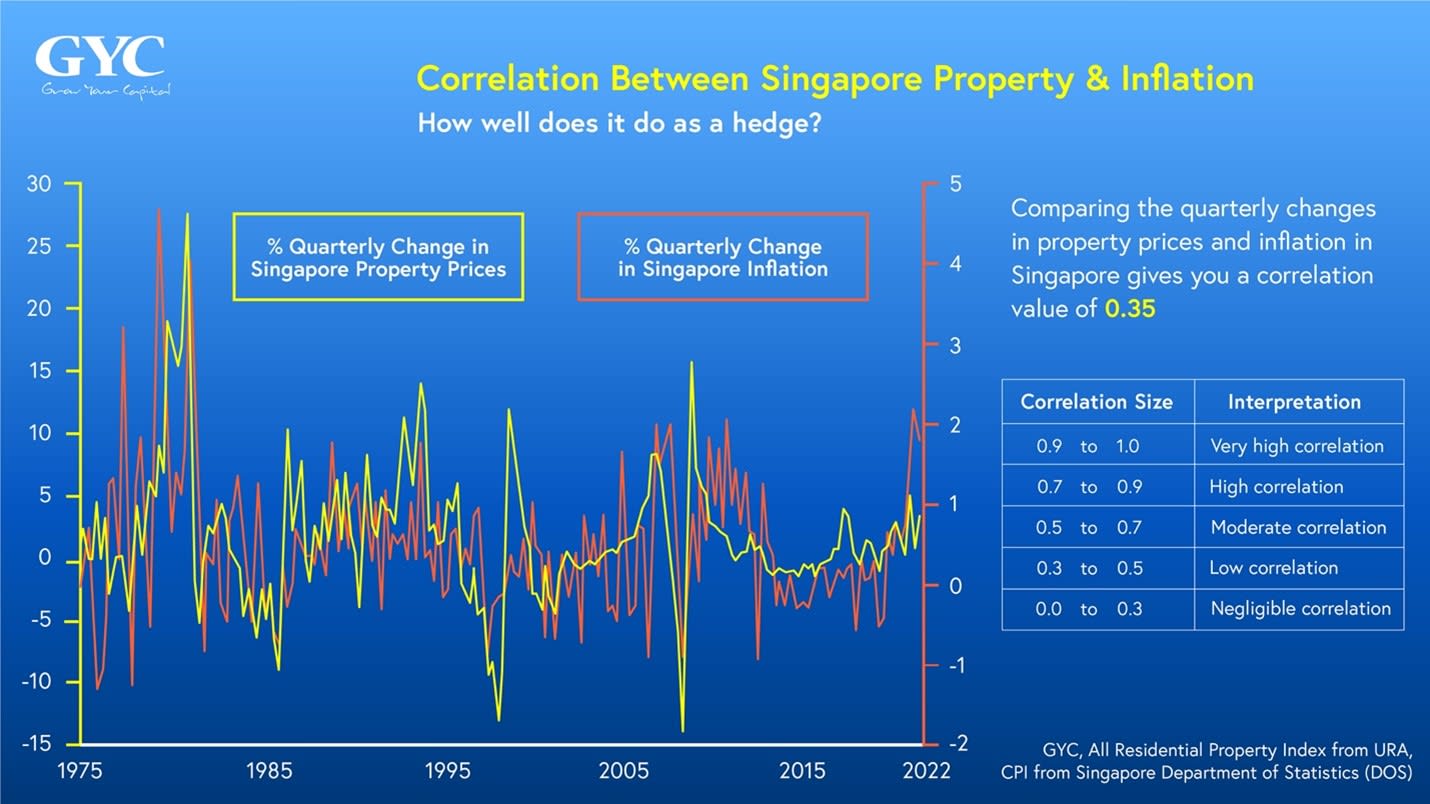

But what does the data show? In reality, the link between inflation and changes in property prices while positive, is pretty weak. For instance, in 1980, Singapore property prices saw an average 18.3 per cent increase over six quarters, whilst inflation remained at a benign 1.6 per cent.

However, looking at quarterly changes can be noisy and volatile and a better way to assess whether there is a strong relationship between two datasets is from the correlation number which we have included in the chart. Owning property may indeed be a hedge, but it is only a weak one.

INFLATION A SLOW AND SILENT KILLER OF PURCHASING POWER

Inflation will continue to be a slow and silent killer of our purchasing power over time.

Unfortunately, most of us tend to have trouble visualising its effects except in periods of spiking inflation when it affects our pockets. It also compounds gradually over a very long period of time.

With increasing lifespans, retirement can last for 20 years to more than 35 years as more Singaporeans cross the centenarian line. Failing to consider inflation in one’s retirement plan may lead to the unfortunate situation where after a decade or more of retirement, you may one day find yourself still alive, but with your retirement coffers empty.

Unless one is endowed with more than sufficient resources, the majority of Singaporeans need to take steps to ensure that their limited resources last for as long as they live, which has an unknown end date.

By employing evidence-based and globally diversified investing strategies, having a retirement income plan that takes inflation into account is not as complicated as it may seem. It requires one to invest time in understanding how everything may play out in the long term, and then taking steps to design an income plan that is not only able to beat inflation in the long run, but also provide sufficient liquidity to tide over short periods of investment volatility.

Aw Choon Hui is the Deputy CEO at GYC Financial Advisory.